.jpeg)

5 min read

Every drafts and review matters

Extract structured data from hundreds of documents at the same time.

Read more

2 days ago

See what serious buyers might pay for your auto repair, collision, or specialty shop - based on how they’re valuing businesses like yours today, not last decade’s rules.

General Auto Repair

From routine maintenance to engine overhauls

Collision & Body

Insurance work, refinishing,restoration & more

Tire & Alignment

Tire shops, brakes, suspension & wheels

Quick Lube & Express

Oil change, fluids, fast-turn services

Detailing & Specialty

Premium appearance & customwork

1

Enter your revenue

Your last 12 months' revenue, or your best full-year estimate. If you're seasonal, annualize accordingly.

2

Enter your profit

Your approximate EBITDA or owner's take-home. If you don't track EBITDA, estimate what you'd keep after paying a manager to run the shop.

3

Select shop details

Choose your shop type (repair, collision, tire, detailing) and number of locations. These significantly impact valuation multiples.

4

Answer profile questions

Quick questions about your growth trajectory, customer concentration, and how involved you are day-to-day.

5

See your estimate

Get a valuation range reflecting how buyers would likely value your business, plus the key factors influencing it.

6

Decide next steps

Save your estimate, identify improvements, or speak with someone who can provide context.

If you Google “business valuation calculator,” you’ll mostly find generic tools: plug in profit, slap on a multiple, and out pops a number. But auto repair and collision are not generic small businesses:

You’ve got insurance programs, OEM certifications, DRP scorecards, and capacity constraints that live and die on cycle time and technician efficiency.

Real estate is often purpose-built, heavily improved, and subject to zoning and environmental rules that don’t apply to a café or e-commerce brand.

The buyer pool includes national and regional MSOs, private equity platforms, local strategics, and real-estate investors - each looking at your shop through a different lens.

And the market has changed. There was a period when great collision shops could reliably get 100%+ of revenue. Today, quality operations in the $5M+ range can still command strong revenue and EBITDA multiples, but buyers are more disciplined and more focused on fundamentals like DRP performance, margins, and workforce stability.

In the automotive industry, value is shaped by:

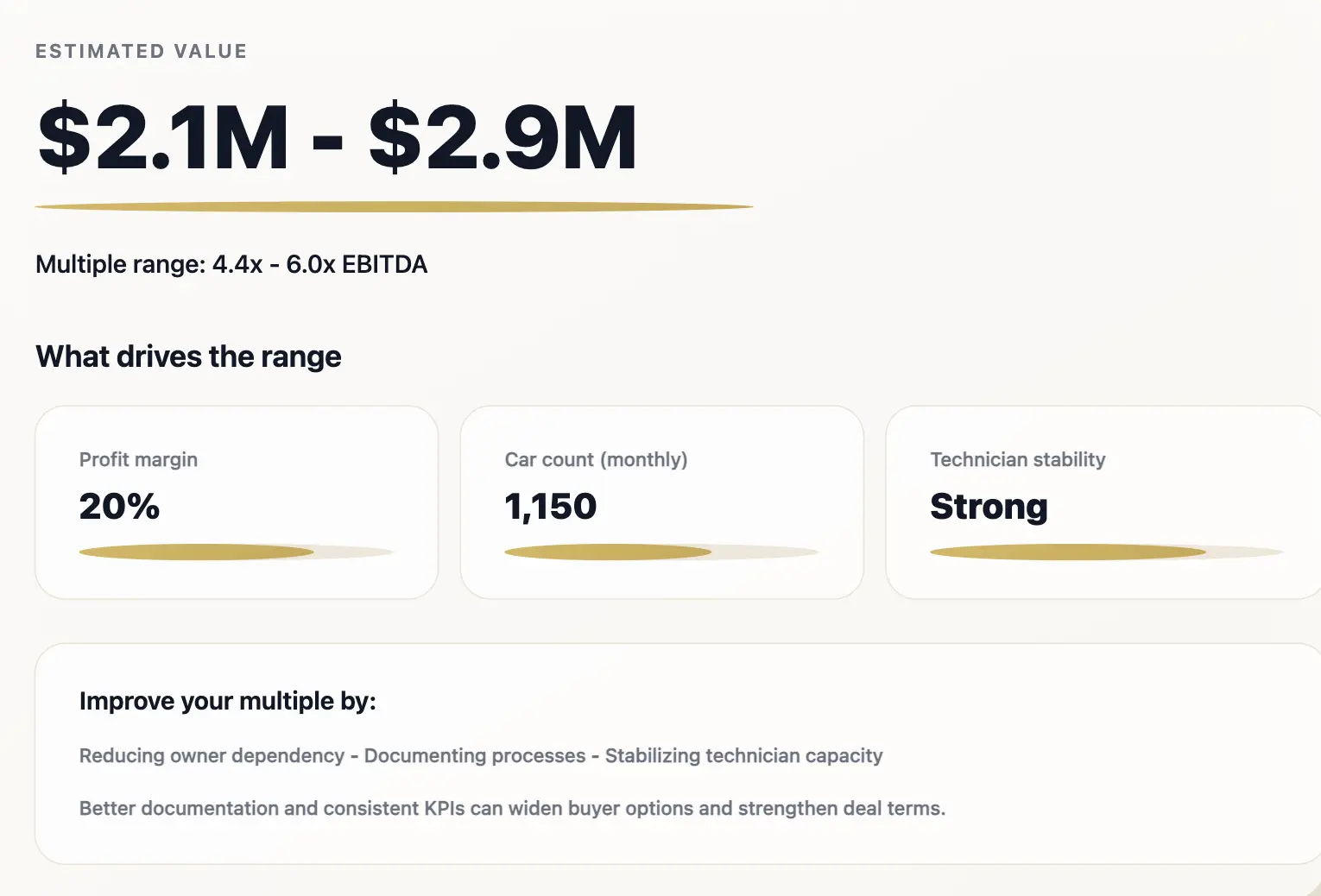

A directional estimate of what your auto repair, collision, or specialty shop could be worth in today’s market, based on the same size bands and multiples serious buyers actually use (revenue %, EBITDA multiples, and where businesses like yours typically trade).

Here’s what’s happening behind the scenes, in the same way a serious buyer would think about it.

First, we ask for:

- Your annual revenue (ideally your last 12 months)

- Your profit, as EBITDA or a best estimate of what you take home from the business.

Under the hood, we treat this as normalized EBITDA, the way buyers look at earnings when they recast your financials:

- Stripping out personal expenses (family vehicles, non-business travel, non-essential perks).

- Resetting owner and family wages to a market salary.

- Excluding one-off items (large, non-recurring costs or windfalls) that won’t repeat.

That gives us a starting point for “how much cash this shop actually throws off” in a way a buyer would accept.

When sophisticated buyers look at a shop, they’re not just asking “What’s the EBITDA?” They’re asking:

In collision, valuation frameworks often break into size bands:

$1–5M revenue: ~30–70% of revenue or 3–5x EBITDA.

$5–15M revenue: ~60–90% of revenue or 4–6x EBITDA.

$15M+ platform-level MSOs: ~80–120% of revenue or 6–10x EBITDA (and higher in competitive processes).

In practice, similar logic applies across auto service, collision, and specialty: as revenue and EBITDA cross certain thresholds, your buyer set changes (local operator → regional MSO → PE-backed platform) and so does the multiple.

One theme that comes up repeatedly with auto-repair shop focused buyers we work with is multiple arbitrage - the idea that two $3M shops worth 3x EBITDA individually might be worth 5x together once they look like a small MSO - 1+1=3.

In collision, valuation frameworks often break into size bands:

There are clear thresholds where the buyer universe expands. For example, around $1M+ of EBITDA and 3 - 4+ rooftops in collision. At those levels, platform PE buyers and larger MSOs become serious bidders.

Those buyers can often “afford” higher multiples because when they buy something at 5–6x and fold it into a platform that trades at 13–15x, the value of that EBITDA instantly steps up on their side.

Even if you’re not trying to build a regional MSO, it’s useful to understand how close you are to those thresholds. It changes:

While still a controversial idea, some countries are experimenting with AI systems.

While still a controversial idea, some countries are experimenting with AI systems.

Echo AI handles repetitive tasks like drafting contracts and reviewing documents.

Echo AI handles repetitive tasks like drafting contracts and reviewing documents.

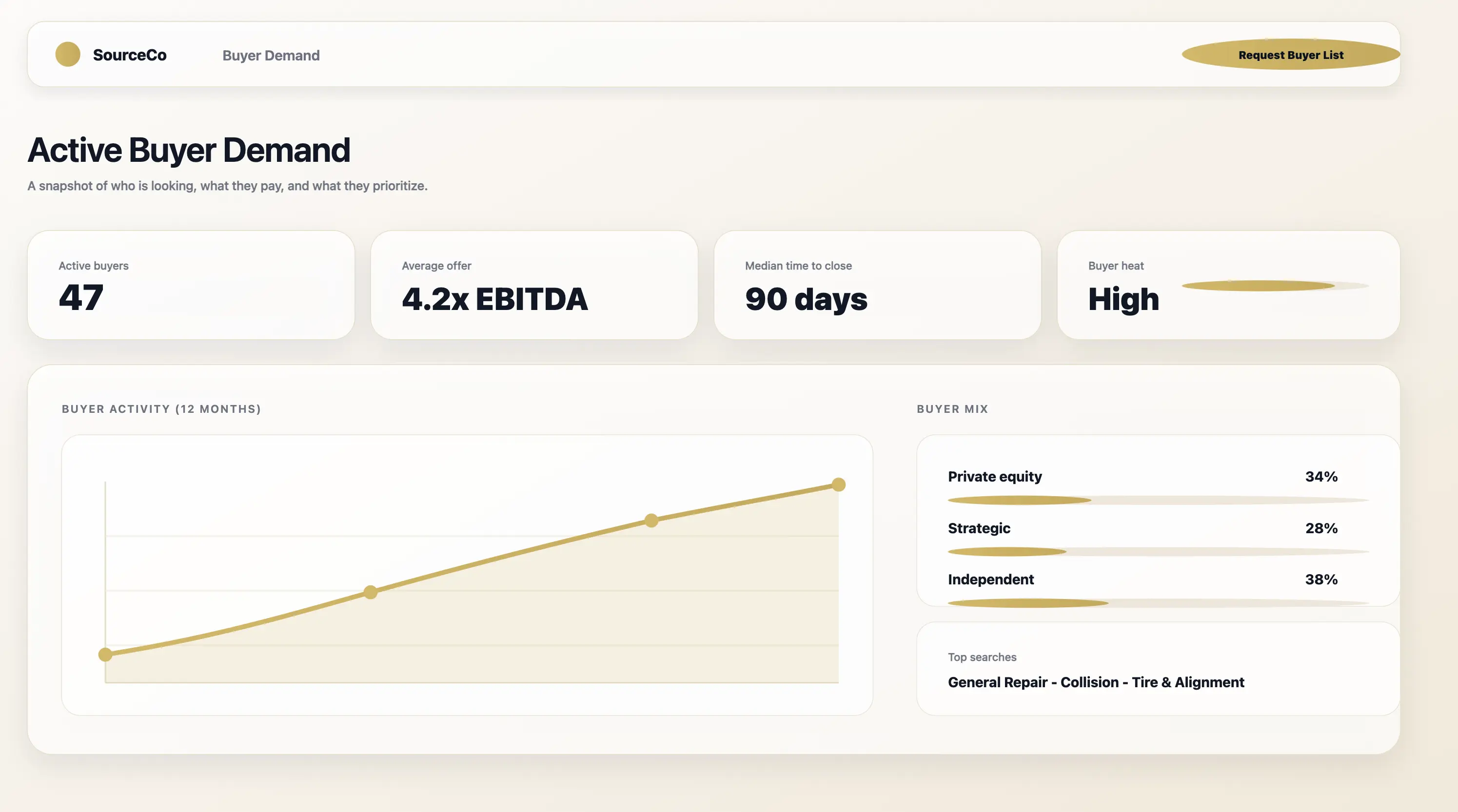

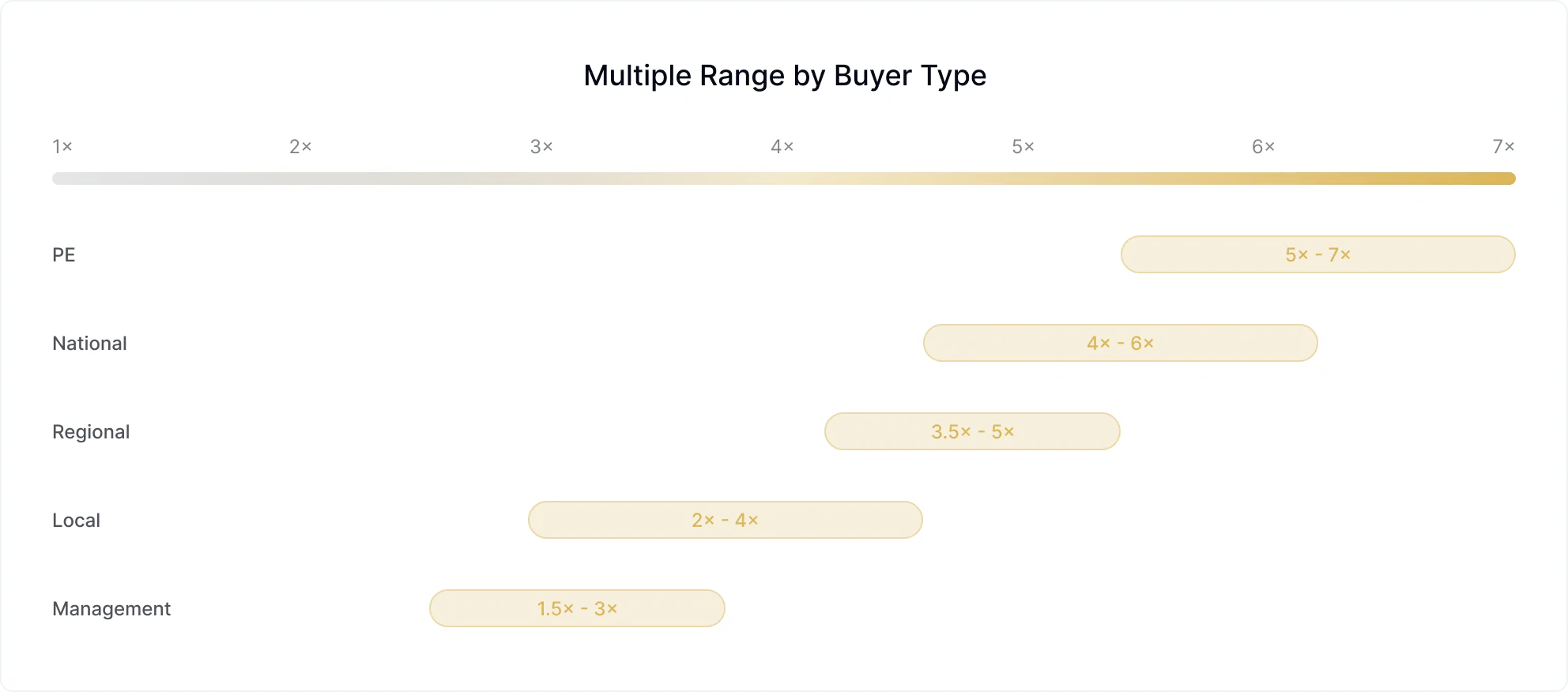

Different buyers see different value. Understanding who's on the other side of the table helps you interpret your estimate and think about positioning.

.png)

National Platforms & Large Consolidators

Large MSOs building national footprints through acquisition

Target Profile

Multi-location operators, strong financials, proven management

What They Focus On

Scale, KPI performance, growth runway, culture fit

Typical Pricing

Highest multiples (4-6x+ EBITDA), but very selective on targets

Regional MSOs & Multi-Shop Operators

Regional players building density in specific markets

Target Profile

Single or multi-location in their geographic focus

What They Focus On

Market position, customer relationships, facility quality

Typical Pricing

Premium multiples (3.5-5x) for strategic fit, standard otherwise

PE / Family Offices

Financial buyers creating platforms or adding to portfolios

Target Profile

Larger shops ($1M+ EBITDA) or groups for platform creation

What They Focus On

Financial performance, management team, growth potential

Typical Pricing

Platform deals at premium (5-7x), add-ons at lower multiples

Local Strategics & Individual Operators

Other shop owners, dealers, or entrepreneurs entering the space

Target Profile

Shops in their area, often smaller deals (<$2M)

What They Focus On

Location, customer base, equipment, real estate situation

Typical Pricing

Market multiples (2-4x), often with seller financing

Management / Family Buyers

Internal transitions to employees or family members

Target Profile

Any shop where succession is the goal

What They Focus On

Affordability, financing structure, transition timeline

Typical Pricing

Often below market, but certainty and legacy matter more

Key insight: Valuation is not "one number." It's a range influenced by which buyer you're talking to. A shop worth 3x to a local operator might be worth 5x to a consolidator filling a geographic gap. SourceCo helps map owners to the right buyer types.

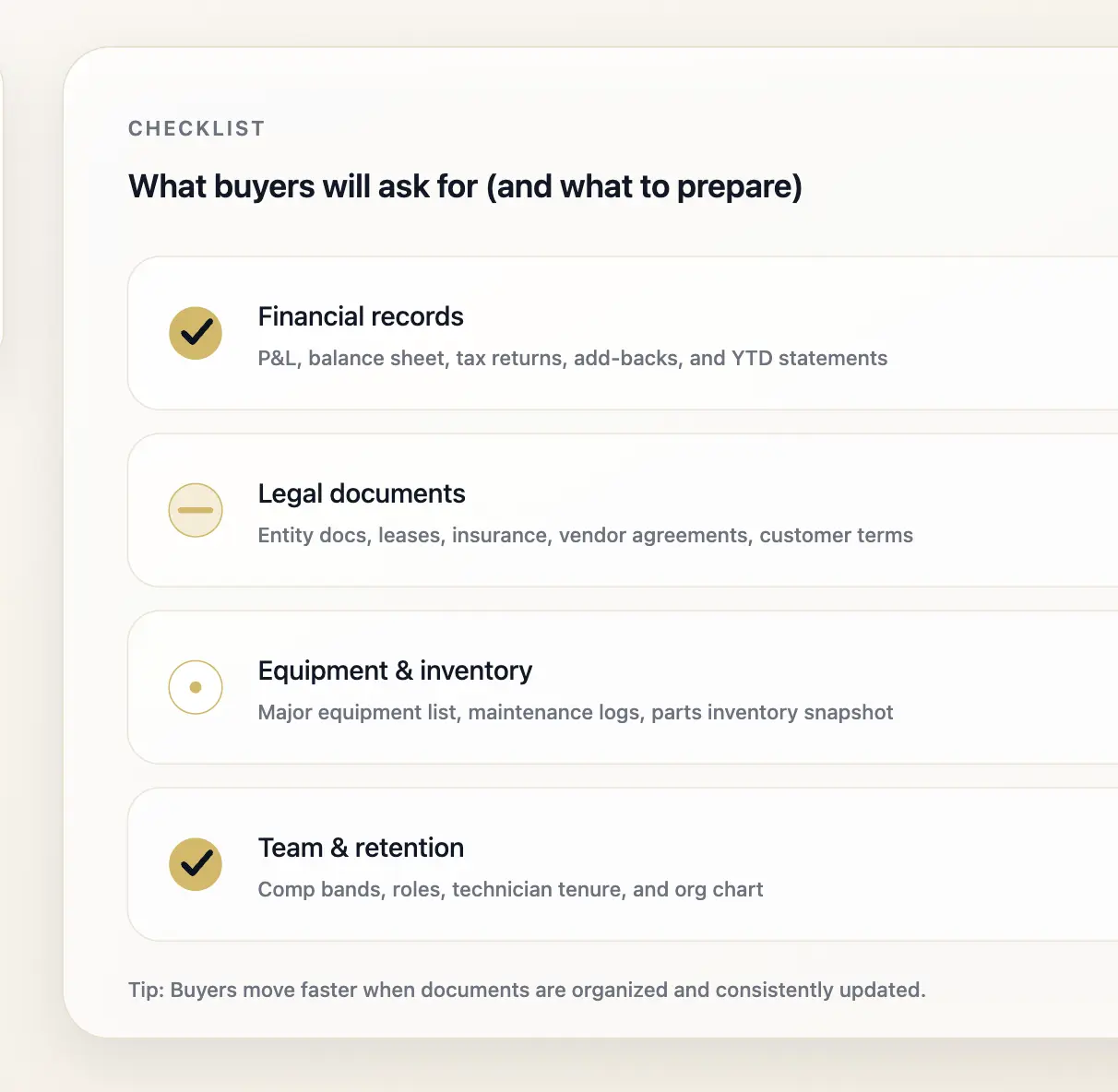

The "price" you hear is rarely what you receive at close. Understanding deal structure is just as important as understanding multiples.

.webp)

.png)

Cash at Close

The portion you receive upfront. Larger deals with stronger financials typically see higher cash percentages.

Typical: 50-80% for larger deals, 60-70% for smaller shops

Seller Note / Financing

You carry a portion of the purchase price, paid out over 2-5 years. Very common in local and management buyout deals.

Typical: 20-40% is standard for single-location deals

Earnout

Additional payments tied to future performance metrics. More common in larger deals or when there's uncertainty about projections.

Typical: 10-25% of total consideration, tied to EBITDA targets

Rollover Equity

You retain ownership in the combined entity. Common when selling to PE-backed platforms who want owner alignment.

Typical: 10-30% for platform deals, rare in local acquisitions

Key insight: A "higher price" with a big earnout and long seller note might actually be worth less than a slightly lower all-cash offer. Always look at deal structure holistically, not just the headline number.

Different exits mean different valuations, structures, and outcomes. Here's the landscape.

Sell 100% to a Strategic Buyer (Local, Regional, or National)

Sell to another operator, competitor, or someone entering the industry. Classic "main street" M&A.

Who is this for

.png)

Owners who want a clean exit with strong cultural continuity

Shops with stable teams, clean books, and transferable DRP / fleet relationships

Collision centers with strong KPIs (cycle time, CSI, capture) or general repair shops with repeatable ARO + utilization metrics

types of strategic buyers

Local operators expanding to 2–8 shops (most active under $1M EBITDA)

Regional MSOs and strong independents (~$500k - $2M EBITDA range)

National consolidators (Caliber, Gerber, Classic) competing for larger or KPI-strong shops

Pros

Typically highest % of cash at close

Cultural continuity for teams

Cleanest personal transition

Cons

Can come with tight integration requirements, especially in DRP-heavy collision

May require you to stay for transition (3–12 months)

Valuation impact: Competitive markets see better pricing; limited buyer pools can suppress multiples

Sell to a Private Equity - Backed Platform

Sell to a platform building scale - MSOs, PE-backed groups, or strategic consolidators. This is where the highest multiples typically live.

Who is this for

Multi-location operators or high-performance single shops with $1M+ EBITDA

Owners open to rolling equity and participating in a second “platform exit"

Why PE-backed companies seek these shops:

Strong leadership benches

SOP-driven operations

KPI excellence (cycle time, CSI, tech efficiency)

Growth runway (more locations, more throughput)

Pros

Highest strategic value (scale, synergy, platform upside)

Opportunity to roll equity and participate in a much larger future exit

Cons

More sophisticated diligence

Heavy focus on EBITDA quality, lease + real estate, and management depth

Valuation impact: Highest potential multiples, but most selective - they want specific profiles.

Sell to an Independent Sponsor or Search Fund

Pass the business to children or relatives. Involves emotional, governance, and financial planning well beyond valuation.

Who is this for

Shops in the $500k–$1.5M EBITDA range

Strong cultural shops where the owner wants the business to continue “as is”

Owners open to seller financing, partial rollovers, or creative structures

Why this can be a fit

Independent sponsors often bring professional management

Are patient with transition timing

Offer flexible structures (seller notes are normal)

Pros

Extreme structural flexibility

Strong cultural alignment opportunities

cons

Usually lower headline cash than PE or consolidators

Heavier involvement required during transition

Valuation impact: Valuation matters for estate planning and buy-sell agreements, but isn't the primary driver.

Internal succession - Management / Employee / Family Buyout

Sell to your trusted team or family. Rewards loyalty and maintains culture, but typically requires heavy seller financing.

who is this for

Owners with a strong second line of leadership (GM, estimator, service manager)

Shops where continuity and team preservation are core priorities

Common structures

Management buyouts with seller financing

Partial buy-ins over time

Transition plans spanning 12–36 months

Pros

Maximum continuity

Predictable transition

Often emotionally easier

Cons

Lower initial liquidity

Heavier financing involvement (banks + seller notes)

Valuation impact: Price may be lower, but certainty and continuity can be worth the tradeoff.

The right exit depends on your goals, timeline, and what matters most to you beyond price.

See how different shop profiles translate to valuation ranges. Use these to pattern-match against your own situation.

.webp)

These are illustrative composites based on market patterns, not actual transactions. Your situation may differ based on specific factors not captured here. Use these as directional guidance only.

Choose your path based on where you are in your journey. There's no wrong answer.

3+ years out

I’m just curious and not selling anytime soon.

Great, this is the ideal time to understand your levers. The guide emphasizes that many of the best-run shops were not prepping for a sale; they were simply run with investor-level discipline. Key steps:

Clean up books 18–24 months before you might sell (stop personal expenses, document add-backs).

Build KPIs into weekly rhythm (cycle time, CSI, tech efficiency, ARO, comebacks).

Reduce owner dependency by delegating estimating, front office, or production.

Planning ahead

I Might Sell in 1 - 3 Years

Shops getting top multiples have years of clean growth and strong culture you can't fake this in 90 days.

Buyers, especially consolidators and PE-backed platforms, value clean operations, stable teams, documented processes, and predictable KPIs.

Normalize payroll (move family off payroll or align comp with market).

Document SOPs so the business runs without you.

Fix lease issues before going to market (renewals, assignability, terms).

Address known environmental items early - they become deal-killers late.

Strengthen management bench (train a GM, or promote a top estimator/tech).

In the market

Actively Considering Offers

At this stage, understanding your buyer pool is more important than optimizing long-term operations.

Your likely lanes depend on your calculator result + profile:

< $500k EBITDA → local strategics, independent sponsors

$500k - $2M EBITDA → regional operators, independent sponsors, select PE micro-funds

$2M+ EBITDA → PE-backed platforms and consolidators (multiple lanes)

Next steps:

Validate your financials.

Map buyer universe by geography & strategy.

Determine best structure (seller note, rollover equity, RE strategy).

These are illustrative composites based on market patterns, not actual transactions. Your situation may differ based on specific factors not captured here. Use these as directional guidance only.

Short, direct answers to the questions collision and auto owners actually ask us and the buyers we work with.

Transparency about how we build these estimates and what they're good for.

.png)

.png)

.png)