Just Launched: The SourceCo Marketplace. Access vetted, off-market founder-led deals before anyone else.

Last deal added: 12 hours ago · Avg deal size: $8.2M · Median revenue: $4.9M

See Live Deals →

No mechanical-repair multiple is published. Here is how buyers actually decide.

Get a free valuation estimate

Enter your site. We'll show you real buyers acquiring in your space. No signup. Confidential.

Show Me →

Takes 30 seconds · No cost

Enter your site. We'll show you real buyers acquiring in your space. No signup. Confidential.

Show Me

Takes 30 seconds · No cost

"I'm kind of on autopilot right now. I don't have to put a lot of effort in to make what I'm making."

That is where most auto repair shop owners are when they start asking about valuation. Not urgency. A shop that works, a number from a broker or a peer, and a need to verify it quietly before doing anything else.

The problem: you cannot test that number without involving someone. And involving someone can start a process the owner did not mean to start.

Your shop's valuation starts with earnings: SDE (Seller's Discretionary Earnings, the total earnings including your compensation) or EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization), multiplied by a multiple based on risk and buyer type, then reduced by debt, working capital (the current assets minus liabilities the buyer requires at close), and deal structure. The number you heard is real only if each of those inputs holds up. Here is how to test it.

A quoted number is not a valuation. It is a shorthand, usually a multiple applied to some version of earnings, and it becomes a real number only after four inputs are verified. Most numbers owners hear collapse when one or more inputs are examined.

[[step-process: 4 steps to pressure-test any valuation number you have heard]]

Confirm which earnings metric was used | SDE and EBITDA are different figures on the same financials. A buyer of a smaller owner-run shop will typically use SDE; a buyer of a larger, manager-run shop often uses EBITDA. If someone gave you a multiple without specifying which earnings figure it applies to, the number is incomplete. Ask: is this multiple applied to my tax return net income, my SDE, or my EBITDA?

Verify what gets added back | A multiple applied to reported net income is not the same as a multiple applied to normalized earnings (SDE or EBITDA after all add-backs are applied and one-time items removed). Owner salary above what a market-rate manager would earn, personal vehicle expenses, depreciation, interest, and family payroll that will not continue post-sale all factor differently depending on how they are handled. The normalized figure can be meaningfully higher than the tax return, or lower if a buyer challenges add-backs (costs that will not continue under new ownership).

Understand what drives the multiple | No published mechanical-repair-specific EBITDA multiple dataset exists in named public form. Multiples depend on buyer type, shop size, technician and customer concentration, lease quality, and operational documentation. A shop with strong systems and low key-person risk will see different multiples than an owner-dependent shop with undocumented earnings. Practical test: ask whoever gave you the multiple to name the comparable transactions they used. If they cannot name them, the multiple is an informed opinion, not a data point. That is not disqualifying, but it tells you how much of the number to negotiate.

Map the bridge from enterprise value to what you keep | Enterprise value (EV, the headline business price before any deductions) is not your check. Debt, working capital shortfalls, transaction costs, and earnout (proceeds contingent on post-close performance targets) holdbacks reduce what lands in your account. A $1.4 million enterprise value can produce $1.0 million at close depending on structure. Section 4 covers this step in full.To make the gap between a rough number and a real one concrete: a shop owner is told by a peer their shop would sell for around $1.2 million. The peer used a 4x multiple applied to $300,000 net income from the tax return. If normalized SDE is $390,000 after proper add-backs, the same 4x multiple produces $1,560,000. If a different buyer uses 3.25x on EBITDA of $340,000, the result is $1,105,000. Three figures from the same shop and the same year. None of them is wrong. All of them are based on different inputs.

[[cta]]

The short answer: it depends on shop size and how the business runs. For smaller owner-operated shops (typically under $3 to $5 million in revenue where the owner is central to daily operations), buyers and advisors most often use SDE.

For larger shops or those with a manager running the day-to-day, buyers move toward EBITDA. Per Quist Valuation's analysis of valuation conventions, the threshold is not rigid and depends partly on the buyer type.

Changing the metric on the same shop's financials changes the headline value before any multiple discussion begins.

[[definition-list: The earnings terms buyers use to value your shop]]

SDE (Seller's Discretionary Earnings) | The total earnings available to an owner-operator: EBITDA plus the owner's full compensation. Used for smaller owner-run shops where the owner's pay is the primary return. Reflects what you personally take home from the business.

EBITDA | Earnings Before Interest, Taxes, Depreciation, and Amortization. Removes financing and ownership-specific decisions, leaving the operating profit a hired manager would generate. Used when the shop can operate without the owner's daily involvement.

Add-backs | Costs on the tax return that a buyer agrees will not continue under new ownership. Owner salary above a market-rate manager, personal vehicle expenses, family payroll not needed post-close, one-time legal fees. Each requires documentation; every dollar of add-backs multiplies directly by the multiple.

Normalized earnings | SDE or EBITDA after all supported add-backs are applied and one-time distortions removed. This is the number buyers actually underwrite.

QoE (Quality of Earnings) | An independent review of whether normalized earnings are accurate and repeatable. Per Doeren Mayhew's pre-sale diligence framework, institutional buyers commission a QoE before any final price commitment. Every add-back is tested. Unsupported add-backs are rejected: at 3.25x, a $30,000 rejected add-back is $97,500 off the headline.The add-backs that survive diligence (buyer scrutiny during the formal verification process after an LOI is signed) and those that do not differ by one thing: documentation.

Add-back type | Accepted when | What weakens it

Owner salary above market rate | Supported by a written market comparison showing what a hired GM would cost | Entire owner salary claimed without a market analysis; no compensation study

Depreciation and amortization | Universal, always accepted by all buyer types | N/A

Personal vehicle expenses | Receipt-level documentation showing personal use portion | Claimed without receipts; vehicle demonstrably used for shop operations

One-time legal fee or facility repair | Invoice confirming the cost was non-recurring | Item appeared in two or more prior years; claimed as one-time without explanation

Family member payroll not continuing post-close | Employment records showing the role, compensation, and confirmation it ends at close | Family member holds an operational title that creates ambiguity about necessityHere is how the metric choice changes the starting point for a real shop:

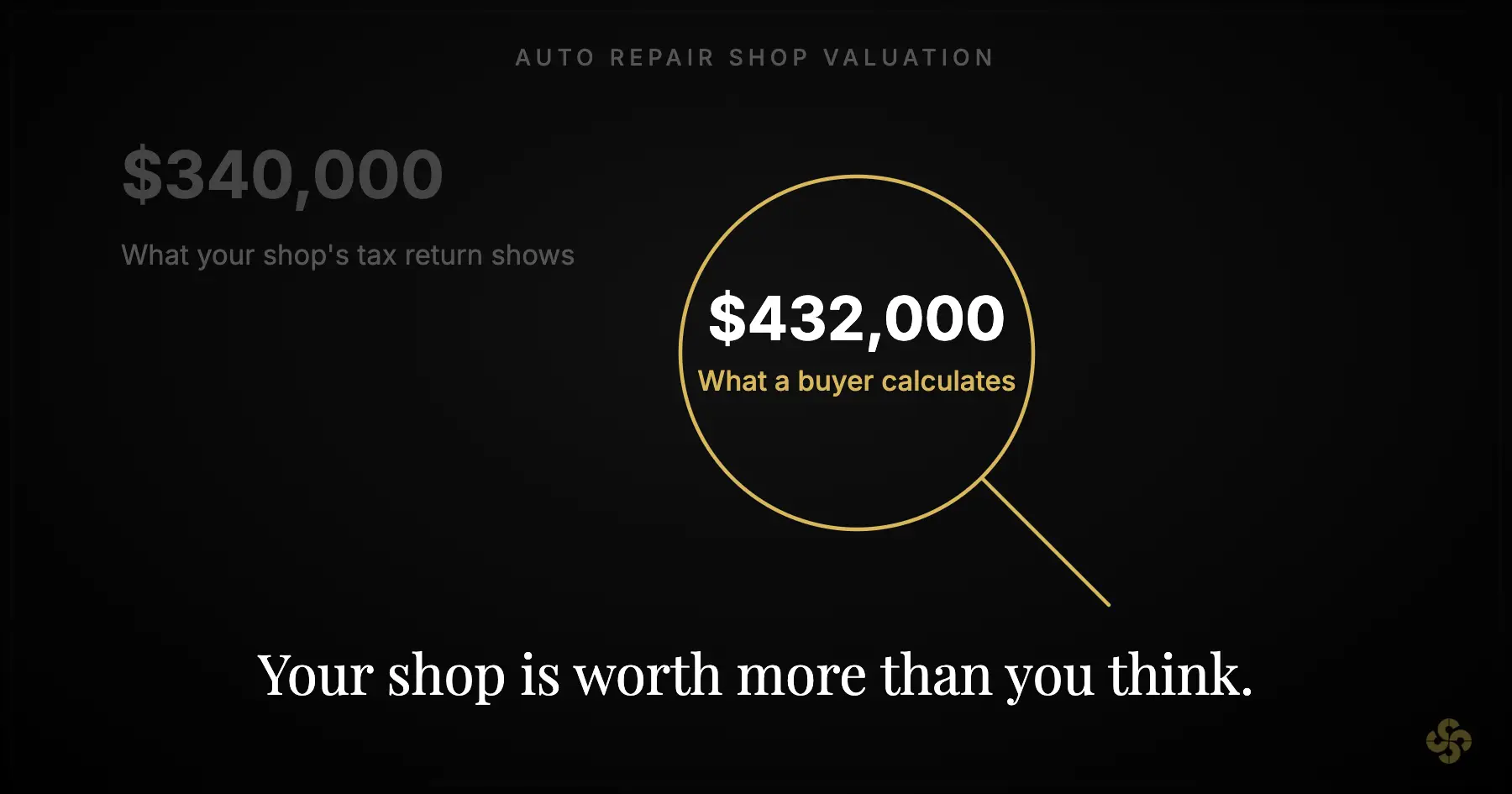

A shop reports $340,000 in net income on the tax return. The owner pays themselves $95,000 in salary. A market-rate general manager would cost $65,000, creating a $30,000 excess salary add-back. A personal vehicle runs through the business ($12,000). Depreciation is $28,000, interest is $7,000. A family member earning $15,000 will not continue post-sale.

Normalized SDE: $340,000 + $30,000 (excess salary) + $12,000 (vehicle) + $28,000 (D&A) + $7,000 (interest) + $15,000 (family payroll) = $432,000.

Normalized EBITDA: $340,000 + $28,000 (D&A) + $7,000 (interest) = $375,000. Owner salary, personal expenses, and family payroll are not EBITDA add-backs.

Same shop. Same year. Same financials. SDE of $432,000 versus EBITDA of $375,000, a $57,000 difference before any multiple. At a 3.25x multiple, the SDE path produces $1,404,000 in enterprise value; the EBITDA path produces $1,218,750, a $185,250 difference at the headline.

An owner who does not know which metric a buyer will use cannot verify whether the number they heard was reasonable.

Buyers pay for repeatable profit they believe will continue after the owner leaves. Two shops with the same revenue and the same reported earnings can produce different offers because buyers see different risks in how that profit is generated.

[[definition-list: KPIs buyers track in a mechanical shop]]

ARO (Average Repair Order) | Average revenue per vehicle visit: total sales divided by car count. Signals whether the shop captures complex, high-value work or primarily handles minor services. Higher ARO with stable car count signals pricing discipline and customer trust.

Effective labor rate | Actual dollars billed per labor hour compared to the shop's posted rate. Reflects how completely the shop converts available labor into revenue. A persistent gap between posted and effective rates signals discounting, declined services, or billing inefficiencies.

Bay utilization | The percentage of available bay-hours generating revenue. Measures whether physical capacity is producing returns or sitting idle. Low utilization with adequate car count typically signals a technician or scheduling constraint.

Technician dependency | The degree to which production, customer relationships, or specialized capability concentrates in one or two people. High dependency means a buyer models the revenue risk if that person leaves.Based on SourceCo's analysis of buyer conversations in automotive services transactions, seven operational factors consistently move the multiple within a given size band:

Factor | What buyers read from it | Impact on valuation

Car count stability, trailing 24 months | Durable demand versus event-driven or cyclical variation. Declining car count signals customer attrition, not seasonality | Declining count triggers earnout conditions tied to count recovery or a lower multiple

Effective labor rate relative to posted rate | Pricing discipline and service writer effectiveness. Gap signals revenue leakage | Persistent gap reduces multiple; strong effective rate supports the upper end

Bay utilization | Whether physical capacity converts efficiently to revenue | Underutilized bays at adequate car count signal a technician problem buyers price into the deal

Technician depth and concentration | Whether production is distributed or concentrated in one or two people | Concentration above 40% in one technician (based on SourceCo's analysis of buyer screens) triggers earnout conditions or price reductions

Fleet versus retail revenue mix | Fleet accounts signal stable recurring revenue but create single-account risk. Retail signals diversification | Single fleet account above 20% of revenue (per SourceCo's buyer analysis) typically results in tighter deal covenants

Warranty and comeback rate | Low comeback rate signals quality execution. Elevated rates indicate rework costs that reduce real margins | Buyers review 12 to 24 months of service data; elevated rates visible in shop management software

Parts margin | Gross profit percentage on parts relative to industry norms. Per Kaizen CPAs' auto repair profitability framework, labor gross margin targets 60-70% and parts gross margin targets 50-55%. | Below-target margins reduce normalized earnings if buyers adjust at diligenceTo make the contrast concrete: two shops both report $400,000 in normalized SDE.

Shop A has a car count steady at 265 per month for 24 months, effective labor rate 91% of posted, three technicians with roughly equal production contribution, no single fleet account above 12% of revenue, and a comeback rate under 3%. A buyer building their model for Shop A is running one calculation: what is the probability that $400,000 in SDE persists in year 2 and year 3 after the owner is gone? Stable car count for 24 months, three technicians each carrying equal load, no fleet account above 12%: the trailing data answers the question without requiring any assumptions.

Shop B has a variable car count (peaked at 305, currently at 230), a single technician driving 52% of production, and one fleet account representing 28% of revenue. The same $400,000 SDE carries more risk because a buyer must model: what happens to earnings if the technician leaves, or if the fleet account renegotiates after the sale?

Both shops have the same earnings. The buyer's offer for Shop B will either carry an earnout tied to technician retention, a lower multiple within the size band, or a tighter working capital target. Not because the revenue is wrong, but because the earnings are harder to underwrite as transferable.

"I have two and three generations of families that come to me."

That kind of customer relationship depth is exactly what separates Shop A from Shop B in a buyer's model. It is not a soft selling point. It is evidence that revenue does not depend on one person, one program, or one contract.

One self-check owners can run before any buyer conversation: EBITDA margin. Based on SourceCo's analysis of buyer conversations, shops with EBITDA margins consistently above 10% appear at the upper end of their valuation range. Shops in low-single-digit EBITDA margins tend to see price adjustments or earnout conditions regardless of revenue size. Margin is not the only variable, but it is the one buyers see immediately.

Different buyer types also apply different weight to these factors. The following frameworks are based on SourceCo's analysis of buyer conversations in automotive services transactions. Evidence for mechanical-specific buyer behavior is adjacent to collision research; these patterns reflect what SourceCo observes, not published benchmarks.

Factor | PE platform | Independent sponsor | Strategic operator | Search fund

Primary screen | Management depth, documented systems, scalable operations | Strong fundamentals; owner dependence tolerated with a credible transition plan | Local market fit, technician and customer relationship quality, geographic proximity | Ability to step into the operating role; clean earnings; manageable key-person risk

What they underwrite | Repeatable earnings at scale; team capability post-owner | Current earnings quality; path to reducing owner dependence | Synergy with existing operations, vendor relationships, staff stability | Clean SDE; defined transition; low single-person production concentration

Transition expectations | 3 to 12 months, defined role | 6 to 24 months, new operator steps in | 3 to 6 months, integrating into existing operations | 12 to 24 months, buyer takes over actively

What they may ask for | Earnout tied to revenue or technician retention | Seller note (a loan from you to the buyer, repaid with interest) on part of the price | Seller note common; simpler deal structure | Earnout or seller note; longer transitionOne reason PE platforms and strategic operators can offer more than individual buyers: they are not modeling the shop as a standalone. Based on SourceCo's analysis of automotive acquisition conversations, the multiple at which a platform values individual acquisitions is typically lower than the multiple at which the platform itself is valued.

That gap is why a PE or strategic buyer can pay above what an independent operator can justify and still create value for themselves. It does not mean the offer is better for the owner: terms, structure, and transition expectations are what determine the actual outcome.

[[cta-match]]

Knowing which buyer type fits before outreach begins is the difference between a 90-day process that closes and one that does not. The mismatch between buyer type and what an owner actually wants from a sale is the most common reason transactions start and stop.

The headline number in an offer is enterprise value: normalized earnings multiplied by the multiple. What lands in your bank account is equity proceeds. The gap between the two is where, in SourceCo's experience reviewing offers with owners, attention is on the multiple at signing. The working capital and earnout lines receive that attention later.

[[definition-list: The EV-to-proceeds terms you will see in any offer]]

Enterprise value (EV) | The headline business price: normalized earnings multiplied by the agreed multiple. This is what the buyer says the business is worth. It is not what you receive.

Net debt | Outstanding loans, lines of credit, and equipment financing that transfer with the business. Subtracted from enterprise value at close.

Working capital peg | The minimum level of current assets (cash, receivables, WIP) minus current liabilities the buyer requires in the business at close. If the actual balance falls short of the target, the shortfall reduces your proceeds directly.

Earnout | Proceeds contingent on post-close performance, paid over time if defined targets are met. Common when technician retention risk, owner dependence, or revenue concentration exists.

Escrow or holdback | A portion of proceeds withheld after close to cover potential indemnification claims. Per Stout Advisors' automotive repair transaction framework, 5 to 10% of the purchase price is typical, released after 12 to 18 months if no claims arise.

Seller note | You lend part of the purchase price to the buyer at a negotiated interest rate, repaid over 3 to 7 years. Common in SBA-financed transactions and when buyers need to bridge a financing gap."It was never numbers... what it came down to is terms."

An automotive services owner who went through a sale put it that way. The multiple was agreed on. The price looked right. What determined the actual outcome was structure: which proceeds were conditional, how long they took to arrive, and what the owner had to do to earn them.

Here is what the proceeds bridge looks like for the shop from Section 2. Normalized SDE is $432,000. A buyer offers 3.25 times, placing enterprise value at $1,404,000.

Step | What it means

Enterprise Value | $1,404,000 (normalized SDE of $432,000 at 3.25x)

Minus: Net debt | Equipment loans and line of credit: -$95,000

Minus: Working capital shortfall | WC target was $72,000, actual was $50,000: -$22,000

Minus: Transaction costs | Legal, advisory, intermediary: -$52,000

Subtotal before earnout | $1,235,000

Minus: Earnout (15% of price, 12-month technician retention target) | -$210,600

Cash at close | $1,024,400That is $379,600 between the headline number and the first check. If the earnout is fully earned over 12 months, total proceeds reach $1,235,000, still $169,000 below the enterprise value. The working capital target was in the LOI from the day it was signed. In SourceCo's experience, attention at signing is on the multiple. The working capital target sits on a different page. It arrives as a real deduction in the closing statement that appears 24 to 48 hours before the close date, after the price felt settled for weeks.

Two offers with the same enterprise value can produce meaningfully different amounts at close depending on earnout size, working capital peg, and escrow terms. Map the full bridge before reacting to any headline number.

[[cta]]

Signing the LOI (Letter of Intent, the document that sets price and key terms before formal verification begins) is not closing. It is also when the owner's negotiating position changes. From the day the LOI is signed, the seller is in exclusivity: no other buyers, no parallel conversations. The buyer has 60 to 90 days to examine everything and, if they find problems, to renegotiate from a position of information advantage while the clock runs.

Deals fall apart in this window, and the most common cause is not bad faith: it is add-backs and earnings claims that do not survive scrutiny.

Documents buyers will request for a mechanic shop:

Financial records

Operational records

Lease and facility

Environmental

Legal and structure

Here is what a retrade (a price reduction after the LOI citing issues found in diligence) costs in real numbers. A shop owner signs a $1,100,000 LOI at 4 times normalized SDE of $275,000. During 60 days of exclusivity, the buyer's quality of earnings (QoE) review finds $40,000 in add-backs that cannot be verified: an owner salary adjustment without a market compensation study, and a one-time equipment cost that recurred in two of the prior three years.

At 4 times, $40,000 in rejected add-backs is $160,000 off the price. The buyer's revised offer is $940,000. The owner has already disclosed their customer list, technician compensation details, lease, and vendor relationships. The retrade is not a tactic. It is the mathematical consequence of documentation gaps that existed before the LOI was ever signed.

The preparation that prevents it: document every add-back before any buyer conversation begins. Per an automotive acquisition industry guide's analysis of valuation factors, shops with reviewed or audited financial statements can command 10 to 20% more than equivalent shops with compiled-only financials. The preparation cost is the same; the valuation impact is not.

Document every add-back before any buyer conversation begins: a market compensation analysis for owner salary, receipts for personal expenses, invoices confirming one-time costs are non-recurring. This is the same work a buyer's QoE accountant will do, done earlier, when fixing it costs nothing.

[[cta-advisor]]

Do buyers ever use a revenue multiple for a repair shop?

Sometimes, but revenue alone can mislead. Buyers may glance at revenue as a quick screen (shops in a given range might trade at a rough percentage of sales), but they price the deal on earnings. A shop with $1 million in revenue and 15% net margins looks completely different to a buyer than one with $1 million in revenue and 5% margins. Revenue multiples are a rough cross-check, not a valuation method. If a buyer quotes revenue multiples without discussing earnings normalization, the conversation has not reached a real valuation.

If I want to stay quiet, how do I test value without tipping off my staff or competitors?

Start by building your own earnings bridge privately: pull your tax return, add back owner salary above market rate, personal expenses, depreciation, and interest. Divide by a conservative starting multiple (3x to 3.25x for a smaller owner-operated shop based on SourceCo's analysis of buyer conversations). That gives a rough enterprise value before anyone else is involved. From there, SourceCo can provide a more precise analysis with your normalized earnings and a brief conversation, with no buyer outreach, no listing, and complete confidentiality at that first step.

Will I have to keep working after the sale to get the full price?

Not always, but some deal structures tie part of the price to what happens after close. An earnout might require 12 months of active involvement to receive 15 to 20% of the purchase price. A seller note means part of the price is repaid over 3 to 7 years rather than at close. If a clean exit is a firm requirement, state that preference before the LOI is signed, not during purchase agreement negotiations after the buyer has completed diligence.

What is the EBITDA multiple for an auto repair business?

No named published dataset isolates mechanical auto repair as a distinct EBITDA multiple category. BizBuySell, which aggregates actual transaction data, and advisory firms like Peak Business Valuation both publish auto repair benchmarks, but neither breaks out mechanical-only EBITDA multiples separately from the broader auto repair category. Multiples depend on shop size, operational quality, key-person risk, and buyer type. Treat any published range as a starting orientation, not a final answer.

How do I calculate the value of my auto repair business?

Start with normalized earnings: add back excess owner salary (with market-rate comparison), personal vehicle expenses, depreciation, interest, and any non-recurring costs, each documented. That is your normalized SDE. Multiply by an estimated multiple: for smaller owner-operated shops, 3x to 3.25x SDE is a reasonable starting range based on SourceCo's analysis of buyer conversations, adjusted upward for strong KPIs and documented management depth. Subtract outstanding debt and estimate the working capital position. The SDE calculation and proceeds bridge in this guide show both steps with real numbers.

What add-backs are typically accepted in an auto repair shop sale, and which get rejected?

Universally accepted: depreciation and amortization, interest expense. Accepted when documented: owner salary above market-rate manager compensation (with a written market analysis), one-time legal or repair costs (confirmed non-recurring by invoice), personal vehicle expenses (with receipts). Commonly challenged: owner salary without a market analysis, costs labeled one-time that recurred in prior years, family payroll where the role appears operational. At 3.25x, a $30,000 unsupported add-back is $97,500 off the headline value. Per Franchise Funding Solutions' add-back framework, documentation is what separates accepted add-backs from challenged ones.

What is the difference between enterprise value and what I take home?

Enterprise value is the headline price: earnings times the multiple. What you receive, equity proceeds, is enterprise value minus net debt, minus any working capital shortfall at close, minus transaction costs, minus any earnout withheld pending post-close performance targets. A $1,404,000 enterprise value, for example, produces $1,024,400 in cash at close after deductions for debt, working capital shortfall, transaction costs, and a 15% earnout. Map the full bridge before evaluating any offer: two offers at the same headline can produce meaningfully different cash at close depending on structure.

Is a business worth 3 times profit?

A 3x multiple applied to normalized SDE is at the lower end of the range SourceCo's analysis of buyer conversations documents for mechanical shops. It is typically associated with owner-dependent shops, thin or undocumented add-backs, or concentrated technician risk. Shops with documented management depth and clean financials tend to command multiples toward the upper end of their size band. The benchmark also depends entirely on the earnings figure: 3x net income produces a very different number than 3x normalized SDE on the same set of financials.

What makes an auto repair shop worth more to a buyer?

Four factors have the most consistent impact on multiple within a size band, based on SourceCo's analysis of buyer conversations: management depth (the shop operates without the owner's daily presence), low concentration risk (no single technician or customer drives 40% or more of production or revenue), documented and supported add-backs (normalized earnings that survive a QoE review), and assignable lease with meaningful remaining term. Documented improvements in any of these before going to market directly affect both the multiple and the deal structure a buyer proposes.

How long does it take to get a valuation for my auto repair business?

A private first-pass estimate requires two inputs: your normalized earnings and a brief overview of the shop's profile. SourceCo can provide an earnings-based range in a single working session: no buyer outreach, no NDA needed at that stage, complete confidentiality. A formal quality of earnings review from an independent accountant typically takes two to four weeks and is usually commissioned after an LOI is signed rather than before it. The private estimate is the right first step before any buyer conversation begins.

Does owning my building change what my auto repair business is worth?

Yes, in two ways. If you own the facility, the transaction may split into two components: the business (valued on normalized earnings) and the real estate (valued separately on property metrics). A sale-leaseback, selling the building to the buyer and leasing it back at market rate, is common and generates proceeds beyond the business price. If leasing, remaining term and renewal options directly affect the offer: buyers discount shops with fewer than five years remaining and no renewal rights. Confirm assignability and remaining term before any buyer conversation.

A broker estimate, a peer's figure, or a calculator output becomes a real valuation only when the earnings metric is confirmed, the add-backs are documented and supportable, the multiple is grounded in a real buyer's criteria for your shop's profile, and the proceeds bridge is mapped from enterprise value to what actually lands in your account.

Most of that work can be done before you talk to a single buyer. Doing it before any conversation starts is the difference between a number that holds up and one that changes during diligence.

[[cta]]

Free Valuation Tool

.svg)

Before you contact a single buyer, get a first-pass estimate of what your shop could be worth. It takes two minutes and requires no outreach, no disclosure, and no commitment to a process.

Get Your Free Valuation

.svg)

Confidential & Free

.svg)

Before you contact a single buyer, get a first-pass estimate of what your shop could be worth. It takes two minutes and requires no outreach, no disclosure, and no commitment to a process.

Talk to an Owner Advisor

Active Buyers

.svg)

Match with pre-screened buyers from our network of 4,000+ active acquirers - see who is looking for a business like yours instantly.

See Who is Buying

.svg)