Just Launched: The SourceCo Marketplace. Access vetted, off-market founder-led deals before anyone else.

Last deal added: 12 hours ago · Avg deal size: $8.2M · Median revenue: $4.9M

See Live Deals →

32 tools. Real pricing. Honest verdicts. The practitioner’s guide to every software category corp dev teams use, from M&A CRM to AI tools.

Start a Target Search

Enter your site. We'll show you real buyers acquiring in your space. No signup. Confidential.

Show Me →

Takes 30 seconds · No cost

Enter your site. We'll show you real buyers acquiring in your space. No signup. Confidential.

Show Me

Takes 30 seconds · No cost

Most corp dev software evaluations take three months and still end in the wrong tool. This guide exists to shorten that to one read.

Eight categories. 32 tools reviewed. Real pricing, honest verdicts, and the conditions under which each tool is right or wrong. No vendor spin. Updated 2026.

Corporate development software covers every tool in the M&A lifecycle: sourcing, pipeline, modeling, data rooms, intelligence, and diligence.

Pricing from vendor documentation, G2 Spring 2025, and practitioner interviews. Reflects early 2026. In a hurry: read the green box at the top of each section.

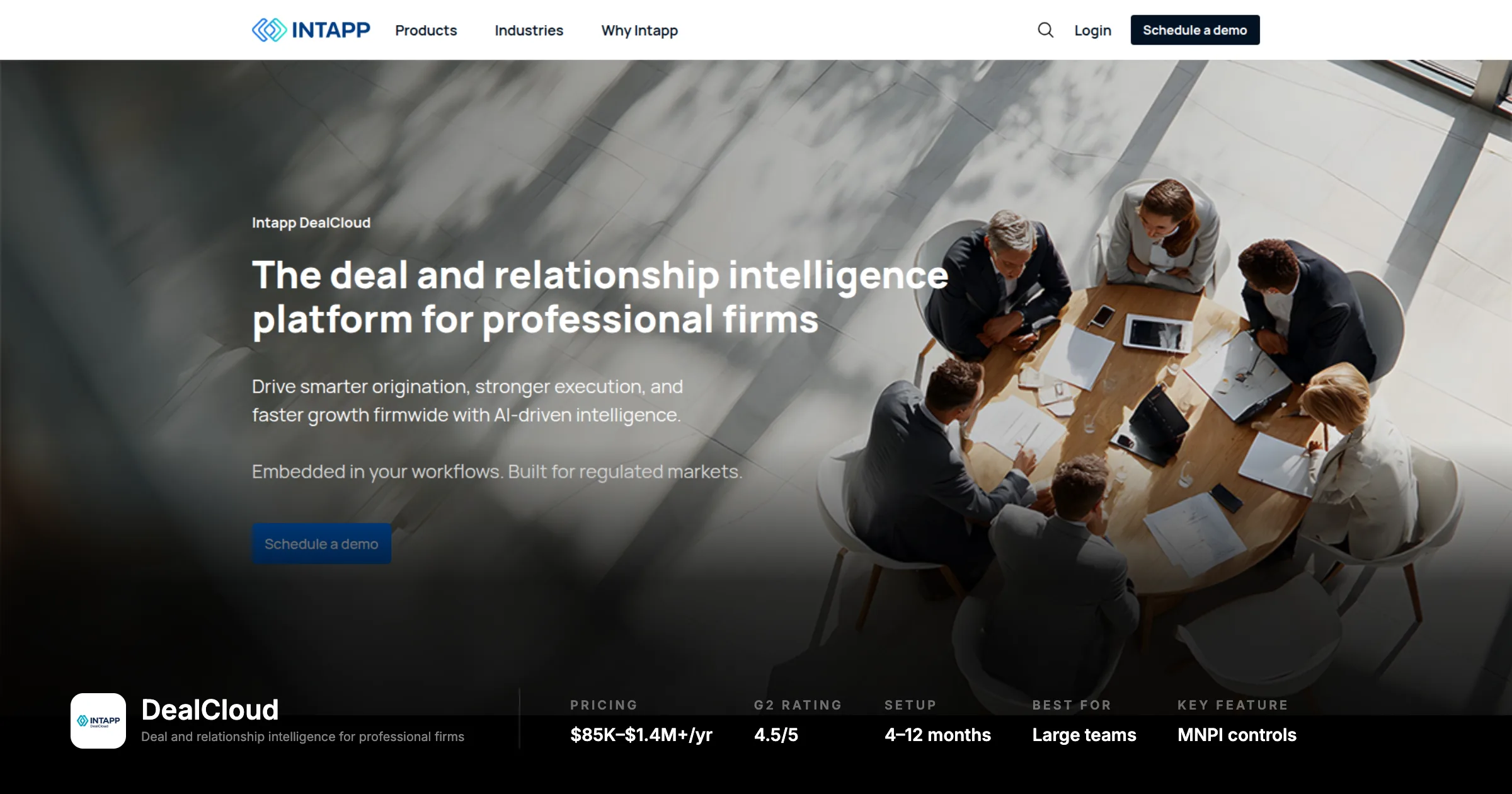

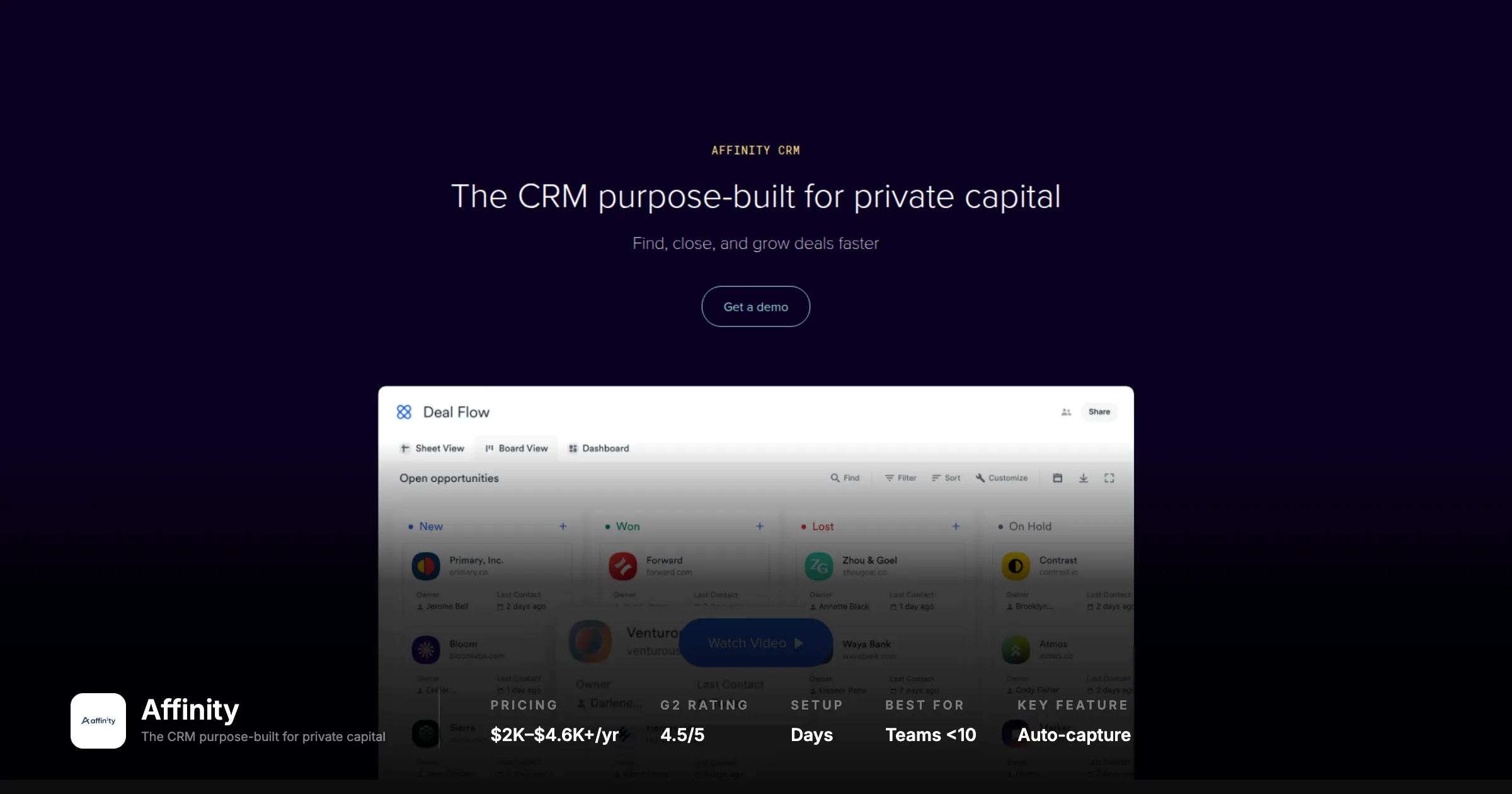

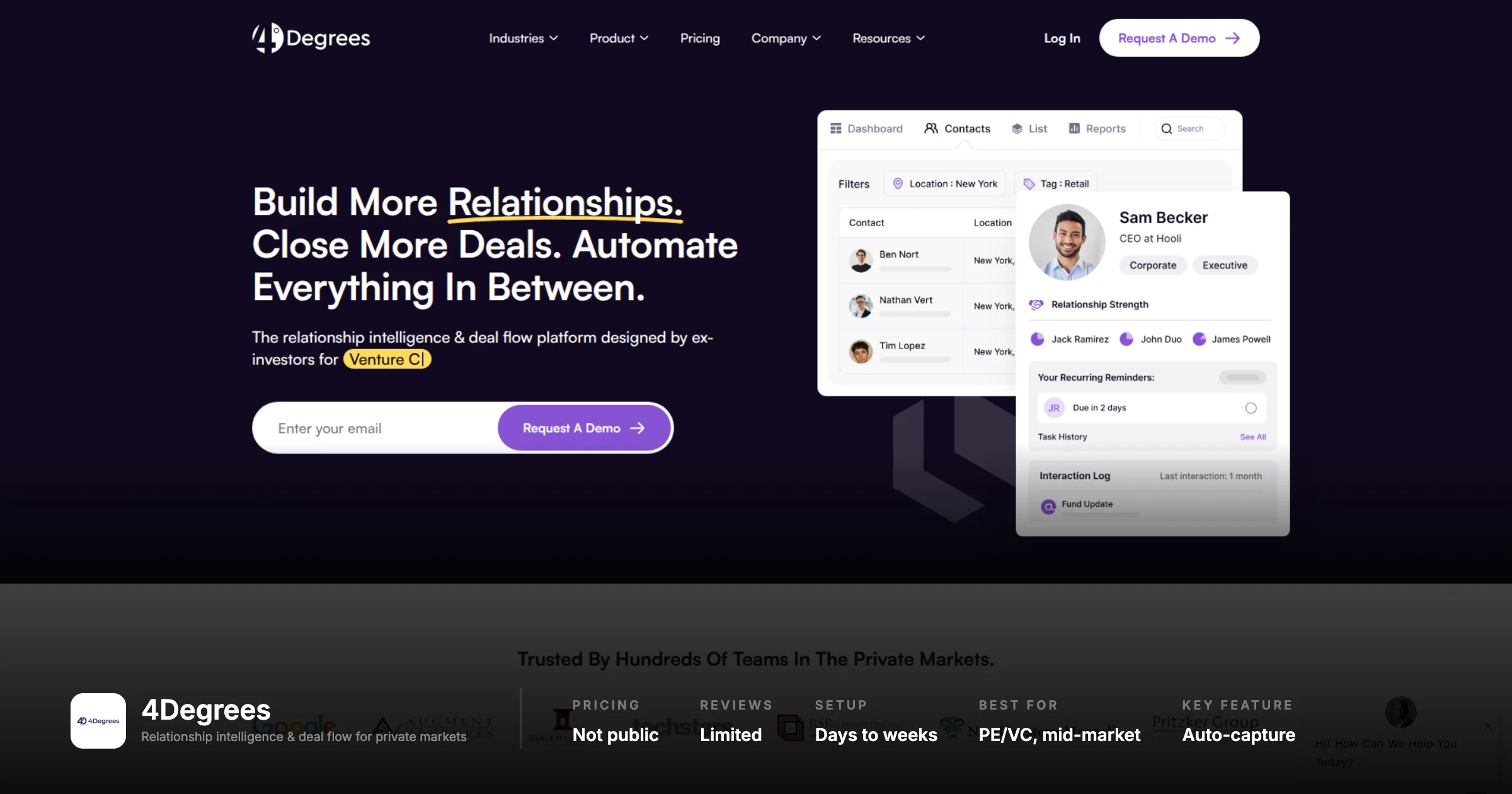

In short: DealCloud for 10+ person teams with compliance requirements ($85K min, avg $505K/yr; 4-12 month implementation). Affinity for teams under 10 where adoption is the primary constraint ($2K-$4.6K+/seat/yr; live in days). 4Degrees if you want Affinity's automation with M&A-native pipeline logic. Midaxo if you need strategy through post-close integration in one platform. DealRoom as a diligence execution layer alongside any CRM. Notion or Airtable for solo practitioners only.

Your pipeline is probably a spreadsheet someone built three years ago, a shared drive folder labelled "Target List Q3," and a series of email threads that constitute your contact history. This is not unusual. It is how 80% of corporate development teams operate, including ones that have closed significant transactions. The question is whether the friction of that setup is costing you deals. What follows is the honest picture of every tool built to fix it.

The real cost of a bad pipeline system is not the time spent on data entry. It is the deal you could not report on in 30 seconds when the CEO asked in a hallway. It is the target you reached out to six months after a competitor did because you had no reminder system.

A corp dev CRM is not a sales CRM. It does not manage lead scoring or automated email sequences. What it needs to do is genuinely different:

With those requirements clear, here is where the available tools land.

Best For Large teams, active acquirers

Pricing $85K-$1.4M+/yr (avg $505K)

Implementation 4-12 months

G2 Rating 4.5 / 5

DealCloud is the closest thing corporate development has to a category standard. Its data model is built for deals: contacts link to companies link to mandates link to transactions in ways that make intuitive sense for M&A. Compliance and information barrier controls are unmatched for public companies handling MNPI. Native integrations with PitchBook and Capital IQ pull market data directly into deal records. The structural problems: no auto-capture from email or calendar (every interaction requires manual logging), any configuration change goes through DealCloud's services team rather than your own admins, and pricing is structurally opaque with professional services layered on top of subscription costs.

"The implementation has been poor and completely missed the mark. The initial promises of being able to guide the implementation with advisory on best-in-class practices fell very short. When the frustration was expressed, the account managers began the blame game."

Verified reviewer, Capterra (non-incentivised)

What practitioners love | What drives them away

Capital markets data model built for M&A, not adapted from sales | No auto-capture from email or calendar: manual entry throughout

Best-in-class compliance and information barrier controls | 4-12 month implementation; any change goes through vendor's services team

Native PitchBook and Capital IQ integrations | Average spend $505K/yr; overkill for teams under 10 people

Customer support consistently praised, including after-hours | Mobile app widely described as functional but frustratingOur Take: DealCloud earns its cost if you have 10+ corp dev professionals, a dedicated CRM administrator, and the patience for a multi-month implementation. At a Fortune 500 with an established deal function, it is the right call. At a 3-person team doing 2 deals a year, it is a $500K lesson in the gap between demo and deployment. The moment your company is not prepared to staff the implementation properly, choose something else.

Best For Teams where adoption is the primary pain

Pricing $2K-$4.6K+/seat/year

Implementation Days to weeks

G2 Rating 4.5 / 5

Affinity reads your email and calendar and builds the relationship record automatically. No manual logging: every email to a target is captured, every meeting recorded, every contact created in the background. The relationship intelligence layer scores relationship strength 1-10 across your whole team, surfacing the warmest path to any target. The ceiling appears when you need serious analytics: reporting below the enterprise tier is underpowered, most users end up exporting to Excel for anything the CEO will see, and the mobile app still cannot create opportunities or edit lists from a phone.

"Analytics lag: sorely lacking versus Salesforce. Limited to aggregates without raw exports. Dashboards need work, frustrating data-heavy teams."

CRMs Reviewed, October 2025 (citing G2 user sentiment)

What practitioners love | What drives them away

Automatic data capture from email and calendar: adoption problem solved | Analytics underpowered below Enterprise tier; most teams export to Excel

Relationship strength scoring actually useful for warm intro sourcing | Mobile cannot create opportunities or edit lists

Fast implementation: days, not months | Built for VC; slight friction in corp dev deal stage logic

AI meeting summaries sync to CRM records automatically (2025) | $2K+/seat before any advanced features unlockOur Take: Best for teams under 10 people doing 5 or fewer deals per year where adoption is the primary problem. The automation is real and the relationship intelligence is genuinely useful. The ceiling appears when you need board-ready pipeline analytics with granular deal data: most users end up exporting to Excel, which somewhat defeats the point.

Factor | DealCloud | Affinity

Team size fit | 10+ professionals | Under 10

Implementation time | 4-12 months | Days to weeks

Contact capture | Manual entry throughout | Automatic from email and calendar

Analytics depth | Board-ready with admin support | Limited below Enterprise tier; most teams export to Excel

Compliance controls | Best-in-class (MNPI, information barriers) | Standard

Price range | $85K-$1.4M+/yr | $2K-$4.6K+/seat/yr

Right if | Compliance is a hard requirement; deal volume is high and admin resources exist | Adoption is the primary problem; team is under 10; setup speed mattersThe deciding variable is team size and administrative infrastructure - not feature preference. DealCloud is built for 10+ person corp dev functions with a dedicated CRM administrator and the budget and patience for a multi-month implementation. Affinity is built for teams under 10 where adoption is the critical constraint. If your team has the budget but not the admin infrastructure, Affinity will be used. DealCloud will not.

Best For PE/VC, mid-market corp dev

Pricing Not public (positioned below DealCloud)

Implementation Days to weeks

G2 Rating 4.7 / 5

4Degrees sits between DealCloud and Affinity in both price and functionality. It auto-captures from email and calendar, includes structured deal pipeline logic that maps to the full investment lifecycle, and offers relationship strength scoring comparable to Affinity. Practitioners who reference it in WSO threads describe it as the option when you want DealCloud functionality without DealCloud pricing or Affinity's VC-centric workflow logic. The honest caveat: fewer independent public reviews from verified corp dev professionals than either competitor. Ask specifically for a corp dev reference before buying, not a VC or PE firm.

What practitioners love | What drives them away

Auto-capture from email and calendar: no manual entry | Fewer independent public reviews than competitors

Deal-practitioner DNA, not adapted from sales or VC | Pricing requires a sales call to discover

Faster implementation than DealCloud | Primary focus is VC/PE; corp dev is a secondary use caseOur Take: Deserves a demo if you are evaluating M&A CRMs and want automation without Affinity's analytical ceiling and DealCloud's price tag. Get a corp dev-specific reference before buying. The logic is sound; the evidence base is just thinner than competitors.

Best For Active acquirers, full lifecycle management

Pricing Not public (subscription-based)

Implementation Weeks

G2 Rating 4.6-4.7 / 5, top-rated M&A platform

Midaxo occupies a different position than the CRM-first tools. Where DealCloud and Affinity are primarily about pipeline and contacts, Midaxo connects the entire M&A lifecycle: strategy alignment, deal sourcing, pipeline, due diligence, and post-merger integration in a single platform. Named a Leader in the 2024 IDC MarketScape for M&A software. For an active corporate acquirer whose operational pain is the fragmentation across sourcing, diligence, and integration tools, this is the most purpose-built solution in the market.

The trade-off: relationship intelligence is less automated than Affinity or 4Degrees. If your primary pain is that relationship history is scattered across inboxes with no central record, Midaxo helps but will not eliminate manual entry as completely. And the reporting module drew specific criticism for being time-consuming and inflexible, which is a significant weakness for a tool whose primary value is centralised visibility.

"Best of breed tool built for M&A. Integrated functionality from cultivation through integration. Reduces admin time. Helps us manage M&A at scale."

Verified corporate development user, G2 2024

What practitioners love | What drives them away

The only tool connecting strategy through post-close integration | Reporting module time-consuming and difficult to customise

Purpose-built for corporate development, not adapted from VC | Relationship auto-capture less sophisticated than Affinity

IDC MarketScape Leader 2024, strong enterprise credibility | Document management needs improvement per multiple reviews

Playbook-driven diligence creates consistency across deals | Pricing opaque; learning curve on initial setupOur Take: If you do more than 3 deals per year and your biggest problem is keeping strategy, pipeline, diligence, and integration connected, Midaxo is the most complete answer in this category. If you do one deal per year and relationship management is the primary need, it is more platform than the problem requires.

Best For Diligence management, deal execution

Pricing $1,250/mo single deal; $12K+/yr pipeline

Implementation Quick; learning curve on advanced features

G2 Rating Positive on UX and customer service

DealRoom's core competency is diligence request management: replacing the shared Excel tracker most teams are still using. It is not a relationship intelligence platform. Pipeline management is present but secondary. What it does well is organise an active transaction: document requests, task tracking, permissions, and team collaboration during a live deal process. Transparent flat-rate pricing is refreshing in a category full of opaque enterprise contracts. Limitations: no mobile app as of 2025, Outlook only with no Gmail integration, and limited top-of-funnel sourcing capability.

What practitioners love | What drives them away

Transparent pricing: $1,250/mo, no per-user ambiguity | No mobile app

Clean diligence request workflow replaces Excel tracker | Outlook only: no Gmail integration

Customer service reputation is exceptional; CEO reads support tickets | Weak on top-of-funnel sourcing and relationship managementOur Take: DealRoom is best used alongside a relationship-first CRM, not instead of one. Use Affinity or 4Degrees for sourcing and pipeline. Use DealRoom when a deal goes active and you need diligence and document management. The pricing makes this combination accessible for most teams.

Every corp dev team will eventually be asked by IT or finance whether the company's existing Salesforce or HubSpot instance can serve as the deal CRM. It can, but configuring either for M&A workflows is an expensive, slow exercise in making a sales tool do something it was not designed for. Salesforce's data model assumes leads convert to opportunities in a predictable sequence. A target you have been cultivating for four years, with three bankers involved and two board-level relationships to manage, does not fit that model. Getting it to fit requires months of custom development and the result is a Frankenstein that your deal team will avoid.

The one exception: if your company is already running a fully staffed Salesforce instance with an internal admin team, and your deal volume is modest (fewer than 5 active processes per year), the integration value with internal systems may be worth the workflow compromise. Do not start from a blank Salesforce instance expecting to build an M&A-ready system without serious investment.

A well-built Notion database or Airtable setup can track deal stages, log contact notes, and produce a pipeline overview that holds up in a board presentation. For a solo practitioner or a first-year function doing one deal at a time, this is not naive: it is fast, cheap, and forces you to understand your own workflow before committing to purpose-built software. The ceiling appears at roughly 200 targets, 10 deal stages, or 5 active processes. Start here if you are building from zero. Graduate when you feel the system buckling under its own weight.

One corp dev director described their homemade Airtable setup as "the best CRM I ever built and the first one I actually use." When their deal volume doubled, they called it "the spreadsheet that ate my life."

Your Situation | Tool to Consider | Why

Large team (10+), high deal volume, compliance requirements, budget available | DealCloud | Enterprise-grade compliance, capital markets DNA, configurable at scale

Small-mid team, adoption is the primary pain, want fast setup | Affinity | Best automation of contact capture, strongest relationship scoring, live in days

Want deal-practitioner logic without DealCloud pricing or Affinity's VC focus | 4Degrees | Auto-capture plus structured deal pipeline; faster and cheaper than DealCloud

Active acquirer needing pipeline through integration in one connected system | Midaxo | Only platform with genuine end-to-end M&A lifecycle coverage

Need diligence management more than relationship management | DealRoom | Transparent pricing, clean execution workflow, strong for active transactions

Solo practitioner or first-year function, limited budget | Notion or Airtable | Start fast, understand your workflow, graduate when you feel the ceiling

Already on Salesforce with internal admins, modest deal volume | Salesforce (configured) | Integration value is real if admin resources exist; do not start from scratchTeam Archetype | Recommended Stack | Budget Range

Solo hire / first-year function | Notion or Airtable for pipeline. HubSpot free tier for contacts. Upgrade when you feel the ceiling. | Near zero to ~$200/mo

Small team, 2-5 people, 5-20 active targets | Affinity Essential or 4Degrees. Automatic contact capture is worth the cost: your CRM will have actual data in it six months from now. | $10K-$25K/yr

Mid-sized active acquirer, 5-15 people | Midaxo if full lifecycle matters. Affinity Advanced or DealCloud if pipeline and relationships are the primary need. | $40K-$200K/yr

Enterprise corp dev function, 15+ people | DealCloud if compliance requirements are real and budget is present. Midaxo if operational pain is in connecting strategy through integration. | $150K-$500K+/yrThe most important CRM decision is not which platform to choose. It is whether your team will actually use it. The best-architected, most expensive deal management system in the world is worthless if your senior professionals keep their deal notes in their email inbox.

Choose the tool your team will log into every day. Choose the one that reduces friction instead of adding it. The tools that win are almost never the most feature-rich. They are the ones that feel like they were built for how you actually work.

In short: PitchBook for VC/PE-backed and publicly disclosed companies ($12K–$70K+/yr). Capital IQ for public comps and Excel-integrated financial data (~$20K–$40K+/seat/yr). Grata for bootstrapped, niche, thesis-driven target discovery. Axial for brokered LMM deal flow from boutique advisors (success fee, no subscription). SourceCo if you want the outreach done for you against a specific lower middle market thesis. No team needs all five - the right two or three, used with a clear sourcing strategy, outperforms any single subscription.

Deal sourcing - also called deal origination - is not one problem. It is five. A financial database, an AI discovery platform, a deal network, a startup intelligence feed, and a full-service outreach firm each solve a different piece. Most teams need two or three. Almost no team needs all five. The expensive mistake is subscribing to tools that overlap and calling the result a sourcing strategy.

A PitchBook license is not a sourcing strategy. A data feed of funded companies is not a target list. Proprietary deal flow comes from a combination of the right data, the right thesis, and direct outreach that creates a relationship before a process begins.

Five categories. Each solves a different job.

Category | What it does | Tools that do it

Full-service sourcing | A firm does the outreach, builds the list, and manages founder conversations on your behalf | SourceCo

Financial databases | Comprehensive data on private and public companies: deal comps, cap tables, investor history, financials | PitchBook, Capital IQ

AI company discovery | Find private companies by what they actually do; surface niche targets a static database would miss | Grata (+ SourceScrub)

Deal networks | Connect with M&A advisors marketing live transactions in the lower middle market | Axial

Startup intelligence | Track funded companies, funding rounds, and market activity, primarily VC and growth-stage | Crunchbase Pro, CB InsightsModel Service, not SaaS

Pricing Monthly retainer + success fee

Contract Month-to-month

Best For Add-on acquisitions, LMM platforms

Disclosure: this section is written in first person because we are describing our own firm. All other sections in this guide are written from an independent perspective.

SourceCo is a buy-side acquisition search firm that combines AI-powered company mapping with direct human outreach to surface off-market targets for corporate development and private equity teams. We are a buy-side search firm, not a subscription platform you log into. The practical difference: instead of handing you a list of companies that match a NAICS code, we build deal-ready target records that capture the fields an IC actually debates before greenlighting an add-on. Does the target serve commercial or residential customers? What portion of revenue is recurring versus project-based? What is the service radius and geographic footprint? How many trucks, locations, or field technicians? Is ownership founder-held with no apparent succession plan? These questions decide whether a company fits your thesis. They do not appear in PitchBook, Grata, or Capital IQ. We pull them from company websites, licensing boards, trade rosters, regulatory filings, workforce data, PPP records, and other public signals, then verify and enrich each record by hand. What you receive is a target set built around the decisions your team actually makes, not a filtered export of whatever a database happens to store.

This is why add-on sourcing is where we do our best work. A platform acquisition tolerates some ambiguity in targeting. An add-on does not: the service mix has to fit, the customer base has to complement, the geography cannot overlap with what you already own. Generic databases return companies that look right on paper and eliminate themselves in the first five minutes of a call. We surface companies where the fit is pre-confirmed before any conversation starts. Brian Nienstedt, Chief Development Officer at NexCore Group (Trinity Hunt Partners), put it directly after a single quarter of working with us: within that time, his team had engaged with 60% of our recommendations and advanced three to due diligence. The number that mattered was not volume. It was that every introduction was a viable candidate. Teams running a buy-and-build strategy in the lower middle market are the primary use case we were designed for.

"SourceCo is a totally different animal than all of the other buy-side firms with whom I have worked in the past. Working with them is one of the best decisions we have made at our platform."

"SourceCo is a totally different animal than all of the other buy-side firms with whom I have worked in the past. Working with them is one of the best decisions we have made at our platform."

Melissa Barry, Partner, New Heritage Capital

What we do differently | Honest limitations

We capture fields databases miss: service mix, commercial/residential split, recurring vs project revenue, footprint, ownership flags | Service model, not self-serve: requires a real thesis conversation upfront, not just a keyword brief

Off-market founder outreach on your behalf, from warmed domains, thesis-personalized, with calling to confirm contacts | Not the right fit for venture-backed or growth-equity targets: our coverage is LMM and founder-owned businesses

AI-built target maps covering bootstrapped businesses with no institutional footprint | Success fee applies on closed deals; total cost depends on deal size

Month-to-month: no annual contract, cancel when the search is complete | Lead times of 2-4 weeks to build the initial target universe before outreach beginsOur Take: If your sourcing problem is that databases give you industry codes and headcount while your IC needs service mix, customer type, and geography before they will approve an add-on, that is the exact problem we were built to solve. Right for corp dev teams doing 2-20 acquisitions per year in the lower middle market, especially those running a roll-up or add-on strategy where fit precision matters more than volume. For private equity firms specifically, our private equity deal flow resource covers how PE-backed platforms approach add-on sourcing differently from corporate acquirers. Not the right model for teams exclusively targeting large, publicly visible, or VC-backed companies.

Best For Mid-to-large corp dev teams

Pricing $12K–$70K+/yr depending on team size

G2 Rating 4.5 / 5

Ease of Use 8.5 / 10 (G2)

PitchBook is the most widely used financial data platform in private capital markets. It has the deepest coverage of private company financials, deal multiples, investor history, and cap tables of any platform in its class. The 2025 Navigator AI feature enables natural language queries across the database. The honest limitation: PitchBook is strong on companies with disclosed history (funding rounds, press releases, investor involvement) and weak on bootstrapped, founder-owned businesses with no public footprint. At $20K-$40K+ per seat, it is hard to justify for teams doing fewer than three deals per year.

"Pitchbook is the best platform for M&A and private placement activities. CapIQ is better for public comps. The two are complements, not substitutes."

Certified Investment Banking Professional, Wall Street Oasis

What practitioners love | What drives them away

Best private market financial data: deal comps, investor history, valuations | Misses bootstrapped, founder-owned businesses with no public footprint

Navigator AI enables natural language market mapping | $20K-$40K+/seat; hard to justify below 3 deals/year

Excel plugin integrates data directly into financial models | Retrospective: shows what happened, not what is about to happen

Covers 3.5M+ companies, funds, and investors globally | UI rated harder to learn than competitors; search logic requires trainingOur Take: Right for any corp dev team doing active deal flow in venture-backed or PE-backed markets, or needing rigorous transaction comp sets. Not a substitute for outbound sourcing in the lower middle market: bootstrapped companies with $5M-$50M revenue are largely invisible in PitchBook. For a comparison of the major private equity data providers, including how PitchBook stacks against Capital IQ and Grata by use case, see our sourcing resources.

Best For Financial analysis, public comps

Pricing ~$20K–$40K+/yr per seat (comparable to PitchBook)

G2 Financial Analysis 9.0 / 10 (vs PitchBook's 7.9)

G2 Ease of Use 7.6 / 10

Capital IQ and PitchBook are the two tools most debated in corp dev circles, and the comparison is mostly a false choice: they are complements, not substitutes. Capital IQ wins on public company financial data. The Excel plugin is the best in the market for pulling standardized financials and building public comp sets. Where it falls short: private company coverage is thinner than PitchBook, the UI is less intuitive for PE-adjacent work, and it lacks the investor-level data (cap tables, fund performance, LP relationships) that makes PitchBook essential for tracking the disclosed private market.

What practitioners love | What drives them away

Best Excel plugin for public company financial modeling | Private company coverage significantly thinner than PitchBook

Stronger index, macro, and sector economic data than PitchBook | UI rated harder to navigate, especially for private markets work

Public comp screening is faster and more reliable for M&A benchmarking | Less investor-level data (fund sizes, LP bases) than PitchBook

Better for carve-outs and public-to-private modeling | Not the right primary tool for bootstrapped or niche sourcingOur Take: Primary deal flow in publicly traded targets or carve-outs: Capital IQ. Primarily sourcing private company targets: PitchBook. Most active corp dev teams end up with both, which is expensive but often justified. If forced to choose one, the answer depends entirely on your deal type.

Best For Thematic, thesis-driven discovery

Database 19M+ private companies

G2 Rating 4.5 / 5 (consistently positive)

Pricing Not public (mid-market SaaS range)

Grata reads company websites like an analyst and classifies businesses by what they actually do, not by NAICS codes. This matters when your thesis is specific: "commercial HVAC companies serving healthcare facilities in the Southeast" requires semantic understanding that static databases cannot provide. Grata's vertical software classification is particularly praised in fragmented tech markets; it distinguishes a CRM built for commercial contractors from one built for state government, where PitchBook tags both as "software." In August 2025, Datasite acquired SourceScrub and is integrating it into Grata, combining SourceScrub's middle-market depth with Grata's AI discovery layer. Agentic Search (late 2025) enables conversational, iterative querying rather than fixed filters.

"CRM integration with DealCloud is miles ahead of others. No other data provider understands vertical software like Grata. When I got recruited to join a new firm, I made it a prerequisite for them to adopt Grata before I stepped foot in the door."

Verified G2 reviewer, PE/corp dev professional

What practitioners love | What drives them away

Best-in-class for niche, thematic market mapping of private companies | Coverage strongest in North America; European and APAC data still developing

Vertical software classification is genuinely differentiated from any competitor | Requires a clear thesis to work well; less useful for broad, undirected prospecting

CRM integrations with DealCloud, Salesforce push targets directly into pipeline | $20K-$60K+/yr; hard to justify without a defined acquisition thesis

19M+ company database including bootstrapped businesses databases miss | Does not show financial data (revenue, EBITDA, valuations) - only descriptive firmographicsOur Take: Right when you have a specific thesis and need to map the full universe of private companies that fit it, including bootstrapped businesses invisible to PitchBook. Turns "here is our thesis" into a list of 400 specific companies. Not a replacement for financial databases or outreach: it builds the list, not the relationship. For a full breakdown of deal sourcing companies by use case, see our sourcing resources.

Best For LMM deal flow, broker relationships

Model Success fee on closed deals (no upfront sub)

Network 20,000+ members, 40–50% LMM deal flow coverage

Deal Focus $5M–$250M revenue, N. America

Axial is a private deal network where boutique M&A advisors market transactions to qualified buyers, confidentially and without public listings. The value is access to the long tail of the advisory market: the 70% of advisory firms that complete three or fewer deals per year, which most buyers are not systematically covering. These are the firms representing founder-led businesses in niche industries that never reach the large investment banks. The trade-off is worth naming clearly: Axial is a marketplace of brokered deals. Multiple reviewers report that listings appear simultaneously on other platforms, and broker responsiveness is inconsistent.

"Axial turbo-charged our business development efforts. More important than the quantity has been the quality. The Axial team created precisely-targeted projects that have yielded one successful closed deal and another in the pipeline."

Verified Axial member, corp dev / strategic acquirer

What practitioners love | What drives them away

Access to boutique advisors not in your network: long-tail LMM coverage | Brokered deals by definition; not truly off-market

No upfront subscription; success fee aligns incentives | Some listings already available on other platforms

Confidential: sell-side controls who sees their deal | Broker responsiveness inconsistent; NDAs signed without CIM follow-through

Good for entering new verticals without an established advisor network | Every deal simultaneously visible to all qualified buyers on the platformOur Take: Legitimate source of deal flow, particularly for teams entering new industries without established advisor relationships. Use it alongside a proprietary sourcing strategy, not instead of one: it is a deal network, which means deals are being marketed to multiple buyers simultaneously.

Best For Tech-adjacent deal sourcing, early research

Pricing $49–$99/mo (Pro) | $199/mo (Business)

Database 3M+ companies, crowdsourced model

G2 Rating 4.5 / 5

Crunchbase Pro is the entry point almost every corp dev team uses before they have budget for anything else. At $49-$99 per month, it provides company profiles, funding round history, leadership data, and search filtering for millions of companies globally. The data model is crowdsourced: well-funded companies have thorough profiles; bootstrapped lower middle market businesses may have skeletal or absent ones. It is built for venture-capital and startup coverage, not for mapping undiscovered operating companies with $10-$100M in revenue.

Our Take: At $49/month, subscribe regardless. The question is whether it is your primary tool, which it should not be: use it for competitive tracking and early screening, then layer in Grata or PitchBook for serious target list building.

Best For Tech company competitive intelligence

Pricing $100K+/yr (enterprise)

Strength AI-written research, market maps

Weakness Breadth of coverage vs PitchBook

CB Insights is a market intelligence platform with analyst-written research, AI-generated market maps, and technology trend tracking. Its mosaic scoring and predictive signals (estimating acquisition and IPO candidates) are more advanced than PitchBook's in that dimension. For a Fortune 500 corp strategy team deciding whether to build, buy, or partner in an emerging technology category, CB Insights produces research that would otherwise require expensive consultants. At $100K+ per year, it prices itself out of reach for most corp dev teams, and its company coverage breadth is materially narrower than PitchBook for deal sourcing.

Our Take: Right for large corporate strategy and corporate venture functions where the primary question is "what is happening in this technology market." For most corp dev teams focused on deal execution, PitchBook plus Grata covers the use case at materially lower cost.

Your Situation | Primary Tool | Why

LMM acquisitions ($1M-$10M EBITDA), want proprietary off-market flow | SourceCo | Founder outreach + AI targeting = conversations no database generates

Need rigorous deal comps, investor data, and market mapping for PE-backed/VC-backed companies | PitchBook | Best private market financial database for disclosed deal activity

Primary workflow is public company financial modeling and benchmarking | Capital IQ | Best Excel plugin; strongest public data layer

Need to find bootstrapped, niche private companies that databases miss | Grata | Reads what companies actually do; 19M+ company coverage

Entering a new vertical without an established advisor network | Axial | Access to boutique deal flow without years of relationship-building

Tracking venture-backed or growth-stage targets on a tight budget | Crunchbase Pro | $49/month; good enough for startup intelligence layerTeam Archetype | Recommended Stack | Budget Range

Solo hire / first-year function | Crunchbase Pro for first-pass research. Grata when you have a thesis to map. SourceCo when you want outreach done for you without hiring a BDR. | $600/yr + Grata/SourceCo as needed

Small team (2-5 people), lower middle market focus | Grata for company discovery. Axial for brokered deal flow. SourceCo if proprietary outreach is a priority. | $25K-$60K/yr

Mid-market acquirer, mix of PE-backed and bootstrapped targets | PitchBook for disclosed deal data. Grata for niche mapping. SourceCo for outreach on priority verticals. | $40K-$100K/yr

Large corp dev function, public company context | PitchBook + Capital IQ. Grata for bootstrapped verticals. SourceCo for targeted outreach programs. | $80K-$200K+/yrThe question that comes up most in LMM-focused teams. These tools are not substitutes - they cover different company populations entirely.

Factor | PitchBook | Grata

Company coverage | VC-backed, PE-backed, companies with disclosed financial history | Bootstrapped, founder-owned, niche private companies; 19M+ companies

Data model | Deal comps, cap tables, investor history, fund performance | What the company actually does; service type, customer, geography - read from website

Discovery method | Keyword and filter search against disclosed data | AI classification of business model and end market

Best for | Comps, market mapping of funded companies, Excel modeling | Thesis-driven discovery of private companies databases miss

Limitation | Blind to bootstrapped businesses with no institutional footprint | No financial data (revenue, EBITDA); descriptive only

Price range | $12K-$70K+/yr | $20K-$60K+/yr

Buy first if | Your sourcing universe is PE/VC-backed or public companies | Your thesis targets bootstrapped founder-owned businesses in niche verticalsEach tool in this category solves a different piece of the sourcing problem. Used together intentionally, they are worth far more than their combined price. Used without a sourcing strategy, they are expensive subscriptions producing target lists that every competitor with the same tools can also access.

The teams with the best proprietary deal flow are not the ones with the most data subscriptions. They are the ones who reached the right founder before anyone else did. For a full practitioner guide to building a sourcing function from scratch, see our private equity deal sourcing guide.

In short: Macabacus is the highest-ROI addition in this category - from $200/user/yr, it reduces model formatting time by 40–50% and eliminates the version-control errors that come with manual Excel-to-PowerPoint updates. Capital IQ Excel Plugin if you regularly build public company comps and precedent transaction tables. PitchBook Excel Plugin if your targets are primarily VC- or PE-backed. Neither data plugin justifies its seat cost for teams exclusively targeting bootstrapped LMM companies. FP&A platforms like Anaplan and Workday Adaptive are the wrong tools for deal modeling - do not evaluate them for this use case.

The financial modeling tool most corp dev teams use is an Excel workbook built for the last deal, maintained in a shared drive, and last properly audited by whoever found the time. This is not failure. Excel is the right tool for deal-specific M&A modeling in most corp dev contexts: every banker, advisor, and board member expects it, every deal has structural quirks no template can anticipate, and the analyst building the model usually needs to defend every cell of it. The case for replacing Excel is weak. The case for making it faster and less error-prone is strong. That is what this category is actually about: tools that accelerate the workflow you already have, not platforms that ask you to rebuild it from scratch. There are four tools worth evaluating and one category of vendors whose pitch you should redirect.

Best For Any team building M&A models in Excel

Pricing From $200/user/yr; enterprise volume discounts

G2 Rating 4.7 / 5

Works With Excel, PowerPoint, Word (Microsoft 365)

Macabacus is the dominant Excel add-in in investment banking and corporate finance, and its adoption in corp dev follows the same logic: it does not replace Excel, it makes Excel substantially faster and less prone to the errors that embarrass people in IC meetings. Formula auditing visually traces precedents, flags hardcoded values in formula cells, and surfaces circular references before the model leaves your desk. Over 100 keyboard shortcuts eliminate the repetitive formatting operations that quietly consume analyst time. The Excel-to-PowerPoint linking earns the most loyalty: changes in your model flow through to linked charts and board deck exhibits without copy-paste, eliminating an entire category of version-control errors every corp dev team has experienced at a bad moment. Practitioners with investment banking backgrounds will recognize the toolset immediately; those who came up through corporate strategy often describe it as the most impactful software change they have made.

"I have probably cut down on my model formatting time by 50%, and my models look better. If my company stopped paying for Macabacus, I would pay for it out of pocket."

G2 reviewer, private equity professional (2025)

What practitioners value | Honest limitations

Formula auditing catches errors before IC; the ROI on avoiding one bad presentation is immediate | Full model-checking runs slow on large files; can take hours on complex multi-tab workbooks

Excel-to-PowerPoint linking eliminates the version-control problem in board presentations | Occasional freeze when tracing precedents in large models; requires Excel restart to clear

100+ shortcuts cut formatting time materially; analysts report 40-50% reduction in formatting work | Keyboard shortcut conflicts with the Capital IQ plugin require remapping on initial setup

Pre-built analysis templates (DCF, accretion/dilution) insert directly into workbooks from a central library | Full feature set has a steep learning curve; most analysts initially adopt 30% of capabilitiesOur Take: The highest-ROI addition available for under $500 per person per year. Right for every corp dev team that builds M&A models in Excel, regardless of size. The only scenario where it does not justify evaluation is if your team delegates all quantitative work to outside advisors and never builds models internally.

Best For Teams building public comps and precedent transaction analyses

Pricing ~$20K–$40K+/seat/yr (plugin included in CapIQ subscription)

Contract Annual; typically 1-year minimum

Also In Part 2 (database and sourcing tool)

Capital IQ was covered in Part 2 as a financial database. Its primary value for many corp dev teams is specifically the Excel plugin, which enables a meaningfully different modeling workflow. Write a CIQ function into a cell and it pulls live data: a comparable company's trailing EV/EBITDA, a target's 8 quarters of historical revenue, an analyst consensus estimate for next year. These cells refresh when you update the dataset, not when an analyst manually re-enters numbers from a browser. For a team building a public company comps table or a precedent transactions analysis, this eliminates 2-4 hours of manual entry per model and removes the version errors that come with it. The value is concentrated in models where public company comparables and disclosed deal data are regular IC deliverables. For teams primarily targeting private lower-middle-market companies with little public comp relevance, the CapIQ subscription's advantages narrow significantly and PitchBook becomes the stronger choice.

Why practitioners use it | Where it falls short

Financial data flows directly into Excel cells; eliminates manual entry for comps and historical financials | High cost relative to value if targets are primarily private companies with thin public comp relevance

Precedent transaction database covers disclosed M&A activity with deal terms and multiples | Private company financial coverage is thin for bootstrapped LMM businesses; data quality only as good as CapIQ's coverage

One-click data refresh keeps comps tables current during live deal processes without manual updates | Hard to justify below 3 active deals per year where the time savings fully materializeOur Take: Right for teams doing 3+ deals per year where public company comps and precedent transactions are a regular IC deliverable. The plugin pays for itself in analyst time within the first two models. Not the right spend for teams exclusively focused on private LMM acquisitions where public comps are thin; PitchBook is the stronger subscription in that context.

Best For Teams targeting VC-backed or PE-backed companies

Pricing ~$12K–$70K+/yr (plugin included in PitchBook subscription)

Contract Annual; multi-year discounts available

Also In Part 2 (database and sourcing tool)

PitchBook's Excel plugin covers a different data universe than Capital IQ's. Where CapIQ is strongest on public company financials and market benchmarks, PitchBook's comparative advantage is private company deal history, investor ownership records, cap tables, and the post-money valuations that define private market transactions. For a corp dev team modeling a VC-backed or PE-backed acquisition, the plugin pulls that company's last three funding rounds, comparable private acquisition multiples, and the ownership structure that informs who you are actually negotiating with. The two subscriptions are complementary: CapIQ for public company data, PitchBook for private market context. Choosing one when budget requires: the decision turns on whether your targets are more often publicly traded peers or private companies with institutional capital behind them.

Where it adds value | Honest limitations

Best private market deal comps for VC-backed and PE-backed targets; pulls directly into Excel | Coverage for bootstrapped, founder-owned LMM businesses is weak; financials often missing or estimated

Cap table and investor ownership data pulls into Excel; useful for mapping ownership before negotiations begin | Navigator AI natural language queries available on the platform but not accessible inside the Excel plugin

Post-money valuation history builds the pricing context section of an IC memo quickly | Pricing is high relative to use if team primarily targets companies with no institutional capital historyOur Take: The modeling data layer to prioritize over CapIQ when deal targets include VC-backed or PE-backed companies with disclosed transaction history. For teams working across both public comp benchmarking and private deal analysis, both subscriptions are justified and complementary. For LMM teams targeting bootstrapped companies, neither plugin solves the data problem; that gap requires sourcing tools, not modeling tools.

Best For Corporate planning and integration modeling, not deal-specific M&A

Pricing Enterprise pricing via Lucanet (custom; was $250/mo standalone)

Status Acquired by Lucanet 2024; repositioned as enterprise product

G2 Rating 4.6 / 5 (pre-acquisition reviews)

Causal earned a strong following among FP&A and startup finance practitioners for a genuinely differentiated idea: replace cell-reference syntax with plain-English variable names, make scenario comparison as easy as toggling a switch, and present outputs as interactive dashboards rather than formatted spreadsheet tabs. It was never built for deal-specific M&A modeling; a merger model or accretion/dilution analysis requires structural flexibility that purpose-built platforms constrain. Where it is relevant for corp dev is in post-close integration planning and multi-year strategic scenario work where scenario management and stakeholder presentation matter more than deal-structure flexibility. The 2024 acquisition by Lucanet, a German enterprise consolidation platform, has repositioned the product away from its accessible, startup-friendly pricing and toward larger organizations with enterprise contracts. Evaluate the current product on its own terms; the reviews that built its reputation predate the acquisition.

Where it works well | Where it does not fit

Scenario toggling and interactive dashboards outperform Excel for planning and integration modeling | Not appropriate for deal-specific M&A models requiring full structural flexibility

Plain-English formula syntax reduces audit complexity on recurring planning models shared across teams | Acquired by Lucanet 2024; the standalone accessible pricing is gone; evaluate the current product, not 2022-2023 reviews

Stakeholder dashboards let boards explore model assumptions without accessing the underlying workbook | Formula syntax differs enough from Excel that existing models do not transfer easily; non-trivial adoption costOur Take: Worth evaluating for post-close integration planning and long-range scenario work where Excel's scenario management limitations are most visible. Not a replacement for Excel in deal execution modeling, and not right for a solo or small corp dev function where deal modeling is the primary workflow.

A note on FP&A platforms pitched as M&A modeling tools: Anaplan, Workday Adaptive Insights, and Planful are enterprise operational budgeting platforms. They are excellent at consolidating business unit data and managing annual planning cycles. They are not M&A deal modeling tools. A deal model is built once, used for 4-8 weeks, requires full structural flexibility, and gets archived when the deal closes. An FP&A platform is configured over months for a recurring data schema and used continuously by a large finance team. If a vendor pitches one of these as a solution to your modeling needs, that is a category mismatch, not a feature.

Your Situation | Primary Tool

Building M&A models in Excel; want fewer errors and faster formatting | Macabacus. Start here regardless of team size or deal volume.

Public company comps and precedent transactions are regular IC deliverables | Capital IQ Excel Plugin. Eliminates manual entry; pays for itself within two models.

Targets are VC-backed or PE-backed; deal comps require private market transaction data | PitchBook Excel Plugin. Better private deal coverage than CapIQ for this use case.

Active across both public comp benchmarking and private deal analysis | Capital IQ + PitchBook. Complementary coverage; not redundant.

Corporate planning and integration modeling alongside deal execution | Causal/Lucanet. Evaluate the current post-acquisition product carefully.

Small team, limited budget, under 3 active deals per year | Excel + Macabacus only. Data terminal subscriptions are not justified at this volume.Team Archetype | Recommended Stack | Budget Range

Solo / first-year function | Excel + Macabacus. Use free trial access to CapIQ or PitchBook when a specific deal requires it; do not subscribe at this volume. | $400-$800/yr

Small active acquirer (2-5 people), LMM focus | Excel + Macabacus for every modeler. Add PitchBook if targets include PE-backed companies with disclosed history. Add CapIQ if public comps are regularly part of IC work. | $2K-$45K/yr

Mid-sized team (5-15 people), mixed deal types | Macabacus enterprise license. Capital IQ for comps and precedent transactions. PitchBook if private deal history is regularly needed. One seat each is sufficient for most teams at this size. | $25K-$120K/yr

Enterprise corp dev (15+ people), integration function alongside deal execution | Macabacus enterprise. Capital IQ and PitchBook. Evaluate Causal/Lucanet for integration tracking and planning if that function sits with corp dev rather than corporate FP&A. | $80K-$250K+/yrThe highest-value modeling decision most corp dev teams can make is not which platform to migrate to. It is adding Macabacus to the Excel setup every analyst already uses, and ensuring whoever builds comps is pulling data from a live connection rather than a browser. Both problems solved for under $50K per year for a team of five, with better ROI than any platform migration in the same timeframe.

Excel will remain the standard for deal-specific M&A modeling for the foreseeable future. The tools worth paying for are the ones that make it faster, less prone to the errors that matter, and better connected to the financial data your IC expects to see.

In short: Datasite for large-cap transactions, investment bank-led processes, and competitive auctions - negotiate flat-rate pricing before the room opens or you will pay per page. Intralinks when post-download document control or cross-border data residency requirements are non-negotiable. Ansarada for sell-side auctions where bidder engagement analytics matter; evaluate the post-Datasite-acquisition product carefully. DealRoom ($1,000/mo flat, unlimited users) for corp dev teams managing buy-side diligence across multiple concurrent acquisitions. SharePoint for internal document staging only - the moment an external party needs access, move to a VDR.

Every serious VDR vendor holds SOC 2 Type II and ISO 27001 certifications. Every one of them encrypts data in transit and at rest. Every one of them offers granular permissions and audit logs. The security credentials that dominate vendor marketing are table stakes, not differentiators. What actually separates the options is less visible and more consequential: the pricing model, the Q&A workflow, the depth of the audit trail, and whether the platform can handle the full diligence workload for a corp dev team running multiple concurrent processes. A typical due diligence process spans quality of earnings review, working capital analysis, legal, tax, and commercial workstreams simultaneously. The most expensive mistake in this category is not choosing the wrong vendor. It is choosing a vendor whose per-page pricing model produces a five-figure invoice you did not see coming, on a deal where you already paid your advisors.

The per-page pricing problem: Datasite and Intralinks still charge per page on legacy contracts, typically $0.40 to $0.85 per page. A 75,000-page deal room at $0.50 per page generates $37,500 in upload fees before a single user logs in. Versioning, reformatting, and reorganizing documents all multiply the page count. According to SRS Acquiom data covering 3,800+ M&A deals, actual costs run 2 to 10 times the initial quote on legacy per-page platforms. Both vendors offer flat-rate contracts on request; you need to ask for them explicitly, and the negotiating dynamic favors the vendor once a deal is already in flight.

Best For Large-cap M&A, investment banks, PE firms running complex multi-party processes

Pricing Custom/quote only; per-page ~$0.60/pg by estimates; expect $25K–$100K+/deal

G2 Rating 4.5 / 5 (332 reviews); value-for-money 4.2 / 5

Certifications SOC 2, ISO 27001, GDPR; ISO/IEC 42001 (AI governance)

Datasite is the category leader on G2's Spring 2025 VDR grid and the default choice for investment banks and large-cap transactions. The platform is trusted by Goldman Sachs, Blackstone, and Johnson & Johnson, which matters in practice because counterparty advisors recognize the interface and arrive with questions about access rather than questions about how the system works. Its AI capabilities are the most mature in the category: automated document classification trained on over three million documents, bulk redaction across 100+ PII types, generative AI summarization, and multi-language OCR covering 16 languages. The Q&A workflow, bulk upload tools, and analytics dashboard are consistently praised in practitioner reviews. The friction points are equally consistent: pricing opacity is the top complaint among smaller teams, the Excel file viewer is limited and frustrates analysts used to working in-app, and per-page pricing on standard contracts makes total cost unpredictable unless you negotiate a flat-rate structure before committing.

"The only con to Datasite is pricing. The legacy providers continue to charge based on page count and special media, while new entrants are offering a flat subscription price based on storage needs."

Verified reviewer, investment banking, Capterra (2025)

What practitioners value | Honest limitations

Category-leading AI: bulk redaction, document classification, and generative summarization all meaningfully reduce diligence prep time | Per-page pricing on standard contracts makes cost unpredictable; negotiate flat-rate structure before deal launch, not during

Institutional recognition: counterparty advisors know the platform and require minimal onboarding | Excel file viewer is weak; reviewers regularly report downloading files to view properly rather than using the in-app viewer

24/7 support team handles administrative tasks including folder structure setup, saving meaningful time on deal launch | Hard to justify for mid-market deals under $50M where document volume is manageable and pricing-per-page punishes smaller teams disproportionately

Analytics dashboard shows reviewer engagement by document, user, and workstream; useful for managing buyer attention in auction processes | Some folder navigation and file-drag actions are non-intuitive; G2 reviewer volume flags this consistently alongside positive overall ratingsOur Take: The right choice for large-cap transactions, auction processes, and any deal where the counterparty team's familiarity with the platform reduces friction. Negotiate flat-rate pricing from the first conversation. Not the right spend for mid-market corp dev teams running $10M to $75M deals where document volume is predictable and the per-page cost structure materially inflates deal costs. To justify internally: frame it around counterparty friction reduction and diligence timeline compression, not security features - every VDR holds the same certifications; the differentiation is workflow speed.

Best For Cross-border deals, regulated industries, processes requiring post-download document control

Pricing Custom/quote only; per-page model; comparable to Datasite at scale

G2 Rating Lower than Datasite on ease of use and value; strong on security

Certifications ISO 27701, SOC 2, GDPR; HIPAA-eligible configurations

Intralinks built the original virtual data room concept and remains the default for global banking and capital markets transactions where regulatory complexity and post-download document control are non-negotiable. Its UNshare technology allows document access to be revoked after download, which no other major VDR matches at the same depth. ISO 27701 certification covers privacy information management specifically, not just information security, which matters for cross-border deals touching EU data or other jurisdictions with strict data residency requirements. The platform's weaknesses are well-documented and consistent across review platforms: the interface is dated compared to Datasite, the admin experience is less intuitive, onboarding external reviewers who are not technology-comfortable creates friction, and costs run high relative to mid-market alternatives. G2 and Capterra reviewers rate it below Datasite on usability while rating it comparably on security and feature depth.

Where Intralinks leads | Known friction points

UNshare post-download document revocation is the strongest IRM capability in the category; critical for processes where information leakage post-exclusivity is a real risk | Interface is noticeably dated; reviewers describe admin tasks as more cumbersome than Datasite on the same workflows

ISO 27701 privacy certification and in-region EU data hosting options serve cross-border deals with strict data residency requirements | Security plugins required for document viewing create technical friction for external reviewers who are not tech-savvy, occasionally stalling diligence timelines

Multi-project management allows deal teams to administer several concurrent VDRs from a single dashboard | Q&A linking capability is limited; reviewers report manually notating document locations in responses rather than linking directlyOur Take: The right choice when post-download document control and cross-border regulatory compliance drive the decision above all else. Not the right choice for teams prioritizing setup speed, modern UX, or predictable pricing. Between Datasite and Intralinks, Datasite wins on usability for most corp dev contexts; Intralinks wins on IRM depth for the specific scenarios that require it.

Both are enterprise-grade, both are expensive, and both use per-page pricing by default. The decision is narrower than the marketing suggests.

Factor | Datasite | Intralinks VDRPro

Market position | G2 Spring 2025 VDR category leader; most recognized by advisors | Legacy standard in global capital markets; stronger in cross-border regulated deals

Post-download control | Standard document permissions | UNshare technology revokes access after download - no other major VDR matches this

Interface | Modern; consistently rated better UX than Intralinks | Dated; admin tasks rated more cumbersome across review platforms

Privacy certification | ISO 27001 (security), ISO/IEC 42001 (AI) | ISO 27701 (privacy information management) - stronger for EU data residency requirements

AI features | Mature: bulk redaction, document classification, OCR across 16 languages | Less developed than Datasite on AI tooling

Right if | Banker or advisor involvement; competitive auction; modern UX required | Post-download document control is a hard requirement; cross-border deal with data residency constraintsBest For Competitive auction processes where bidder engagement analytics drive process management

Pricing Storage-tiered; from ~$479/mo (250 MB) to ~$2,499/mo (4 GB); absurdly tight storage limits

Ownership Acquired by Datasite, Aug 2024 (~AUD $240M); brand operates independently for now

G2 / Capterra Capterra 4.8 / 5 (highest among major VDRs pre-acquisition)

Ansarada's most differentiated capability is its AI bidder engagement scoring, which predicts buyer intent from document viewing patterns and flags which parties are genuinely engaged by day seven of an auction process. Independent evaluators report high accuracy. The platform also offers Smart Sort for AI-powered document classification, a deal readiness scoring tool that surfaces missing materials before a process launches, and a free preparation phase that allows teams to organize the data room before paying for external access. The significant caveats: the storage-tiered pricing model charges $479 per month for just 250 megabytes of storage, which is punishing for document-heavy deals and feels genuinely absurd in 2025. More importantly, Datasite acquired Ansarada in August 2024 for approximately AUD $240 million. The brand currently operates independently, but long-term product roadmap and pricing strategy are uncertain under new ownership. Reviews predating the acquisition should be read as historical context, not current evaluation.

Genuine differentiators | Real concerns

Bidder engagement scoring identifies which parties are seriously engaged; reduces time spent managing disengaged buyers in auction processes | Storage-tiered pricing at $479/mo for 250 MB is the most restrictive cost structure in the category for document-heavy deals

Free preparation phase allows full data room organization before paying; useful for teams building diligence readiness before a formal process | Datasite acquisition (Aug 2024) creates product uncertainty; evaluate the current product directly, not pre-acquisition reviews that drove its 4.8 Capterra rating

Deal readiness scoring and missing-document detection reduce the scramble in the first week of a formal sale process | Long-term independent product roadmap is unclear; integration into Datasite's platform may change feature availability, pricing, or brand continuityOur Take: The bidder engagement analytics are genuinely useful for competitive auctions, and the free preparation phase lowers the cost of getting organized before a process launches. Evaluate the current post-acquisition product carefully before committing; the pricing model is punishing for document-heavy deals and the ownership transition creates real product uncertainty. Right for sell-side auction management. Not right as a primary corp dev buy-side diligence tool at current storage pricing.

Best For Corp dev teams managing multiple concurrent acquisitions with active diligence workflows

Pricing $1,000/mo flat (billed annually); unlimited users; Diligence or Pipeline plans

Contract Annual; Outlook integration only (no native Gmail)

G2 Rating Strong among corp dev practitioners; less reviewed than enterprise VDRs

DealRoom was covered briefly in Part 1 as a deal execution tool. It belongs in this section because it is the most relevant option for a corp dev team that needs both VDR functionality and active diligence project management in one place. Where Datasite and Intralinks are built for sell-side document sharing with passive buyer access, DealRoom is built around the buy-side workflow: a pipeline tracker, structured diligence request lists assigned to counterparty contacts, milestone tracking, and integration planning templates that extend the tool's usefulness past close. Pricing is flat at $1,000 per month for unlimited users, which makes total cost predictable regardless of document volume or deal count. The trade-off is that DealRoom's security features are meaningful but not at the depth of enterprise VDRs; counterparty advisors on large-cap transactions will sometimes push back on using it in place of Datasite or Intralinks. It is also Outlook-only on email integration, which creates friction for teams using Google Workspace.

Why corp dev teams choose it | Where it falls short

Flat-rate pricing at $1,000/mo for unlimited users eliminates the per-page cost unpredictability that plagues enterprise VDRs | Counterparty advisors on large-cap deals sometimes require Datasite or Intralinks; DealRoom is less recognized in sell-side processes

Diligence request lists with assignee tracking replace the spreadsheet-based request management most corp dev teams run in parallel with their VDR | Outlook-only email integration; Google Workspace users lose native email connectivity

Integration planning templates extend the platform's value past close, covering a phase most VDRs do not touch | No mobile app; desktop-only limits accessibility for deal teams traveling during active processesOur Take: The strongest choice for a corp dev team running two or more active acquisitions simultaneously and tired of managing diligence requests in a separate spreadsheet next to their VDR. Right for buy-side-driven processes where your team controls the data room setup. Not right for processes where counterparty advisors or investment banks control the room selection, or for teams that need the security depth and institutional recognition of the enterprise platforms.

Best For Internal diligence prep and document staging before a formal process

Pricing Included in Microsoft 365 subscription (most enterprises already pay for it)

Limit External access controls are weak; no dedicated Q&A audit trails are insufficient for M&A

Works With Microsoft 365 ecosystem; Teams, Outlook, OneDrive

SharePoint is the honest answer to "do we actually need a VDR for this?" For purely internal diligence work, initial document collection, and pre-process organization, it works and costs nothing incremental. The case for using it ends the moment external parties need access. SharePoint's permission model was not designed for M&A: it cannot match the granular user-level document controls that VDRs provide, its audit trail is insufficient for tracking reviewer activity in a formal due diligence process, and it has no Q&A workflow. Sharing documents via SharePoint link with an acquisition target's management team, external counsel, or financial advisors creates real access-control risk and produces no defensible record of who reviewed what. Teams sometimes use it for early-stage diligence requests with known, trusted counterparties on small deals; this is defensible if the deal is genuinely low-stakes and the documents are not highly sensitive. Any process involving investment bankers, formal advisor engagement, or documents you would be uncomfortable having leaked requires a purpose-built VDR.

When it is a legitimate option | Where it fails in M&A contexts

Internal document staging and pre-process organization before a formal VDR is opened; zero incremental cost | External access controls are inadequate for M&A granular user-level permissions that VDRs provide do not exist in SharePoint

Early-stage document collection from internal business units familiar with the environment | No Q&A workflow; coordinating diligence questions via SharePoint produces inbox chaos or a separate email thread that is not tied to documents

Works as a document staging area that feeds into a VDR once external parties are engaged | Audit trail is insufficient; tracking who accessed what document and when is not production-ready for a formal M&A processOur Take: Use SharePoint for internal document collection and pre-process staging. Move to a purpose-built VDR the moment external parties are involved in reviewing sensitive materials. Attempting to run a formal diligence process through SharePoint to save on VDR costs is a false economy; the access-control and audit-trail gaps create risks that are not worth the savings.

Your Situation | Primary Tool

Large-cap M&A investment bankers or PE advisors involved; institutional credibility matters | Datasite. Negotiate flat-rate pricing before deal launch.

Cross-border deal; post-download document control is a hard requirement; regulated industries | Intralinks. The only platform with IRM depth comparable to the use case.

Competitive auction process; bidder engagement analytics drive process management | Ansarada. Evaluate current post-acquisition product; watch the storage pricing closely.

Buy-side corp dev team; 2+ active acquisitions; diligence request management is the primary pain | DealRoom. Flat-rate pricing; covers diligence through integration planning.

Small deal, internal-only diligence prep, or document staging before formal process launch | SharePoint. No incremental cost; transition to a VDR before external parties engage.Team Archetype | Recommended Stack | Budget Range

Solo / first-year function, deals under $25M | SharePoint for internal prep. DealRoom for active diligence processes where you control the data room. Datasite only if counterparty advisors require it. | $0-$12K/yr

Small active acquirer (2-5 people), LMM or mid-market | DealRoom as primary VDR and diligence management platform. Datasite per-deal when investment bankers or advisors require institutional platform. SharePoint for internal document staging. | $12K-$40K/yr

Mid-sized team (5-15 people), mixed deal sizes including large-cap | Datasite as primary VDR with flat-rate annual contract. DealRoom alongside for buy-side diligence tracking if request management is a persistent pain. Ansarada for competitive auction sell-side processes. | $40K-$120K/yr

Enterprise corp dev (15+ people), active seller program or frequent large-cap transactions | Datasite under enterprise flat-rate contract. Intralinks if cross-border regulatory complexity is a regular factor. DealRoom for buy-side pipeline and integration management separate from formal VDR processes. | $80K-$250K+/yrThe VDR decision is simpler than the vendor landscape makes it look. For large-cap processes involving investment bankers and formal advisors, use Datasite and negotiate flat-rate pricing. For buy-side diligence management on multiple concurrent deals, DealRoom outperforms any enterprise VDR at a fraction of the cost and covers the workflow gap between document sharing and actual diligence coordination. For everything else, SharePoint handles internal prep until external parties need access.

The one thing worth repeating: per-page pricing on standard Datasite and Intralinks contracts is the single largest preventable cost in this category. Ask for flat-rate pricing in the first vendor conversation, not after the deal room is already live and you are negotiating from a position of zero leverage.

In short: AlphaSense for teams doing serious sector research and public company competitive diligence - 450M+ documents, cited AI summaries, 240K+ expert call transcripts from Tegus. Start with the two-week free trial before committing to a seat ($10K–$50K+/yr). Bloomberg Terminal only if capital markets, treasury, or large-cap public company M&A independently justify the $24K–$27K+/seat cost. Crayon and Klue are sales battlecard tools - route them to product marketing if there is a use case, not to corp dev. Before subscribing to anything in this category, audit what PitchBook and Capital IQ already cover for your deal types; most LMM teams are underusing what they pay for.

Competitive intelligence software splits into two markets sold under the same name. The first is built for product marketing and sales: tools like Crayon and Klue that monitor competitor websites, generate battlecards, and alert sales reps to pricing changes. The second is built for investment research and corporate strategy: tools like AlphaSense that index SEC filings, earnings transcripts, broker research, and expert call libraries. Corp dev teams regularly evaluate tools from the first category and cancel within a year because the product was built for a workflow they do not run. If you already subscribe to PitchBook or Capital IQ from Parts 2 and 3, audit what those platforms already cover before adding a dedicated intelligence subscription; for most LMM teams the overlap is significant enough to defer.

Best For Corp dev and strategy teams doing deep sector research and public company competitive diligence

Pricing $10K–$50K+/seat/yr; enterprise custom pricing; 2-week free trial available

Scale Used by 85% of S&P 100; $500M ARR (2025); acquired Tegus for $930M

G2 / TrustRadius Consistent category leader; #8 CNBC Disruptor 50 (2025)

AlphaSense is the most relevant tool in this category for corp dev teams. Its search engine spans 450 million+ documents: SEC filings, earnings transcripts, broker research from 1,700+ sources, trade journals, and following the 2024 Tegus acquisition, 240,000+ expert call transcripts covering competitors, suppliers, customers, and sector specialists. A corp dev analyst building a sector thesis for IC can query all of it in one place. The AI features are production-grade: Smart Synonyms surfaces results that exact-term search misses, and generative summarization cites sources rather than hallucinating, which matters when the output feeds an acquisition memo. The weakness is the same as every platform in this guide: private company coverage on bootstrapped or founder-owned businesses is thin. That gap requires the sourcing tools from Part 2, not a better research platform.

"AlphaSense is like having Google for professionals. The breadth of content and AI search across filings, transcripts, and broker research in one place replaced three separate subscriptions for our strategy team."

TrustRadius reviewer, corporate strategy, Fortune 500 company (2025)

Why corp dev teams use it | Where it falls short

Single search across filings, transcripts, broker research, and expert calls; replaces multiple separate subscriptions for research-intensive teams | Per-seat pricing at $10K–$50K+/yr is hard to justify for teams doing fewer than 5 research-intensive deals annually

240,000+ expert call transcripts from Tegus add qualitative sector intelligence unavailable in pure data platforms | Private company coverage on bootstrapped or founder-owned businesses is thin; sourcing tools fill that gap, not AlphaSense

AI summarization with cited sources is defensible for IC memos; does not hallucinate on financial content the way general-purpose AI tools do | Learning curve is real; new users typically underutilize the platform for the first 60-90 days

Customizable alerts surface relevant filings and earnings commentary on tracked companies without manual monitoring | Enterprise Intelligence (internal document search) requires integration configuration; not plug-and-playOur Take: The right tool for corp dev teams running 5+ transactions per year in defined sectors where sector thesis development and public company competitive diligence are regular IC deliverables. For smaller or more generalist teams, PitchBook or CapIQ likely covers enough research ground to defer this cost. Start with the two-week free trial before committing to a seat.

Best For Corp dev functions that include capital markets, treasury, or large-cap public company M&A

Pricing ~$24K–$27K+/seat/yr; multi-seat enterprise discounts available

Launched 1981; standard in investment banking and capital markets globally

AI Status Generative AI features added 2024-2025; behind AlphaSense for research depth

Bloomberg Terminal's dominance in live pricing, fixed income data, FX, and real-time deal news is legitimate and uncontested. The question for corp dev is whether that dominance maps to the work the team actually does. For functions that include treasury responsibilities, capital raising, or significant public company M&A where live market data is a daily requirement, Bloomberg is often already justified on those grounds alone. For teams focused on private company acquisitions and sector research, the cost is difficult to justify: most of its value is in real-time data flows corp dev strategy work does not need, and its competitive intelligence and document research capabilities trail AlphaSense. Its generative AI features, added in 2024-2025, have not closed that gap in practitioner comparisons.

Where Bloomberg leads | Where it falls short for corp dev

Unmatched real-time data: pricing, fixed income, FX, commodities, and market-moving news in one terminal | $24K–$27K+/seat is hard to justify purely on competitive intelligence grounds if capital markets data is not a daily requirement

Universal in investment banking; counterparty advisors use it, so screen-sharing and data references in calls are frictionless | AI features lag AlphaSense on document research and summarization depth for the strategy-grade research corp dev teams need

Excel add-in integrates live market data into financial models for public company analyses requiring real-time comparables | Famously steep learning curve; analysts without investment banking backgrounds lose meaningful time getting proficientOur Take: Worth the cost if capital markets responsibilities, active treasury management, or large-cap public company M&A are part of the function. Not the right primary evaluation for competitive intelligence if those use cases do not apply; AlphaSense covers the research workflow better at comparable or lower cost for teams without real-time data needs.

The comparison that comes up most for enterprise corp dev functions. They are not substitutes - they are built for different primary workflows.

Factor | AlphaSense | Bloomberg Terminal

Primary workflow | Document research: filings, transcripts, broker research, expert calls | Real-time market data: pricing, fixed income, FX, commodities

AI research depth | Best-in-class: cited summaries traceable to source; 240K+ expert call transcripts (Tegus) | Generative AI added 2024-2025; trails AlphaSense on research summarization depth

Price | $10K–$50K+/seat/yr | ~$24K–$27K+/seat/yr

Corp dev research use case | Sector thesis, competitive diligence, IC memo support | Live comps, trading data, banker communication (frictionless because advisors use it)

Right if | Sector research and document intelligence are regular IC deliverables | Capital markets, treasury, or large-cap public M&A are part of the function