Just Launched: The SourceCo Marketplace. Access vetted, off-market founder-led deals before anyone else.

Last deal added: 12 hours ago · Avg deal size: $8.2M · Median revenue: $4.9M

See Live Deals →

Get an estimate to understand your shop's approximate value.

Get a free estimate

Enter your site. We'll show you real buyers acquiring in your space. No signup. Confidential.

Show Me →

Takes 30 seconds · No cost

Enter your site. We'll show you real buyers acquiring in your space. No signup. Confidential.

Show Me

Takes 30 seconds · No cost

A tire shop is valued on normalized cash flow: SDE (Seller's Discretionary Earnings, total earnings including owner compensation) or EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) multiplied by a multiple based on shop size, risk, and buyer type. That produces enterprise value (EV, the headline business price before any deductions). What you receive at close is EV minus debt, minus any working capital shortfall (the gap between the buyer's required current assets minus liabilities and your actual balance), minus transaction costs, and minus any inventory adjustment (a reduction based on the physical count and aging of your tire inventory) applied at closing. The number you heard may be real, but only if whoever gave it to you accounted for all four of those inputs. Here is how to verify each one.

A valuation number becomes real only after four assumptions are checked. Most numbers owners hear fail at least one. The owner does not need urgency to verify a number. But the number needs to be real when the time comes.

[[step-process: 4 questions to verify any tire shop valuation number]]

Which earnings metric was used? | SDE and EBITDA are different figures calculated from the same financials. A smaller owner-operated tire shop where the owner is central to daily operations typically gets valued on SDE. A larger shop with a manager running day-to-day may be valued on EBITDA. Ask specifically: is this multiple applied to my tax return net income, my SDE, or my EBITDA? If the answer is net income, the number is understated.

Which add-backs were applied and documented? | Add-backs (costs that won't continue under new ownership) move normalized earnings, and therefore the headline price, significantly. Excess owner salary, personal vehicle expenses, depreciation, and interest are all standard. But each requires documentation. A buyer's quality of earnings review will challenge every add-back without a supporting receipt or payroll record.

How was inventory treated? | Tire shop inventory is a physical asset worth $100,000 to $200,000 or more in a typical shop. Many valuations state a headline number without specifying whether inventory is included, excluded, or subject to adjustment at close. If it was not addressed explicitly, the treatment is unresolved.

What is the working capital target, and where does your shop currently stand? | Working capital (the current assets minus current liabilities the buyer requires in the business at close) is set by the buyer in the LOI. If your shop's actual working capital falls short of that target at close, the shortfall reduces your proceeds dollar for dollar. Many owners learn the target for the first time when they see the closing statement.The gap between a rough number and a defensible one is widest at questions three and four. Inventory treatment and working capital are the two variables most likely to appear as surprises at the closing table because they are stated in the LOI and then tested at close, not resolved at signing.

[[cta]]

SDE and EBITDA are not interchangeable. Applied to the same tire shop in the same year, they produce different numbers, and both can be correct depending on the buyer type and the size of the shop.

Here is what the difference looks like on one shop's financials.

A tire and mechanical shop reports $220,000 in net income on its federal tax return. The owner pays themselves $85,000. A market-rate general manager for a shop of this size would cost approximately $55,000, creating a $30,000 excess salary add-back. The owner runs a personal vehicle through the business ($8,000). Depreciation is $22,000, interest is $5,000.

Normalized SDE: $220,000 + $30,000 (excess salary) + $8,000 (vehicle) + $22,000 (D&A) + $5,000 (interest) = $285,000.

Normalized EBITDA: $220,000 + $22,000 (D&A) + $5,000 (interest) = $247,000. Owner salary adjustment, personal expenses, and family payroll are not EBITDA add-backs.

Same shop. Same year. SDE of $285,000 versus EBITDA of $247,000: a $38,000 difference before any multiple. At 3.25 times, that gap becomes $123,500 in headline value from the same set of financials.

The normalized earnings (SDE or EBITDA after all supported add-backs are applied and one-time distortions removed) is what buyers actually underwrite. For a deeper look at how this calculation works across mechanical shops, see our auto repair business valuation guide. For a tire shop where the owner is also the service manager or parts manager, the add-back calculation requires a market salary comparison, not just the owner's stated salary.

Service mix also affects which metric applies. A tire shop where service labor generates 60% or more of gross profit is closer in profile to a mechanical shop than to a tire retailer. Buyers evaluating a service-heavy tire shop may use EBITDA rather than SDE, particularly if management depth is strong enough that the owner's role can be replaced.

The enterprise value is the headline business price: what the buyer says the business is worth before any deductions. What you receive is EV minus everything that comes off at close.

In a tire shop transaction, inventory sits in a different category than in a mechanical shop. Mechanical shops carry some parts inventory, but tire shops often hold $100,000 to $200,000 or more in product. That inventory is a variable with real closing-day consequences.

[[definition-list: Inventory and working capital terms in tire shop transactions]]

Inventory adjustment | A reduction to proceeds at close based on the difference between the target inventory value and the actual count. Buyers may apply a haircut to slow-moving or aged inventory: tires in the shop for more than 12 months may be valued below book, and some models may have no agreed buyer value at all. The adjustment amount is determined at the physical inventory count, typically within a few days of close.

Working capital true-up | The adjustment at close when actual working capital differs from the buyer's target. The working capital peg is set in the LOI and tested at close. If your actual working capital is $17,000 below the target, $17,000 comes off your check.

Supplier program | A brand-authorized dealer agreement with a major tire manufacturer that determines pricing tiers, rebates, co-op marketing support, and inventory return terms. Many supplier agreements require the incoming owner to requalify. If the buyer does not qualify for your current program, the inventory purchased under that program may not transfer at the same value.The two adjustments that most affect what you actually receive at close in a tire shop transaction are the inventory adjustment and the working capital true-up. Both are set during diligence and applied at the closing statement that arrives 24 to 48 hours before the scheduled close date, after the multiple was agreed on weeks earlier.

"There's no profit in tires as far as I'm concerned. Tires just opened the door to find other work on the car."

That is from an automotive services owner in the tire segment. It captures the earnings reality that buyers will examine: in a shop where tire margin is thin and service labor is the real earner, the inventory count at close affects proceeds, but the earnings quality that drives the multiple is in the service bay, not on the tire rack.

Here is what the same $900,000 headline produces under two inventory scenarios. In both cases, SDE is $270,000, the multiple is 3.33 times, net debt is $45,000, the WC peg is $95,000, actual WC is $78,000, and transaction costs are $35,000.

Scenario A (fresh inventory) | Scenario B (40% inventory aged >12 months)

Enterprise value | $900,000 | $900,000

Minus: Net debt | -$45,000 | -$45,000

Minus: WC shortfall ($95K peg, $78K actual) | -$17,000 | -$17,000

Minus: Inventory aging adjustment (40% of $180K book) | None | -$72,000

Minus: Transaction costs | -$35,000 | -$35,000

Cash at close | $803,000 | $731,000Both shops were valued at $900,000. The difference is $72,000, applied at the closing statement when the physical inventory count is reconciled against the agreed target. That number was not visible at the time the multiple was discussed.

[[cta-advisor]]

No named published dataset isolates tire shop EBITDA multiples as a distinct category. BizBuySell, which aggregates actual transaction data, and advisory firms like Peak Business Valuation and Dealstream both publish automotive and tire business benchmarks. None provides a named dataset with stated sample size and date specific to tire-only EBITDA multiples.

| Source type | What it tells you | What it does not tell you |

| Advisory firm ranges (Peak BV, Dealstream) | Directional ranges based on advisory experience and rules-of-thumb | The buyer, shop size, inventory quality, or service mix behind any specific transaction |

| Transaction aggregators (BizBuySell) | Average sale prices across listed businesses by category | Whether the transactions were asset or stock sales, how inventory was treated, or what the normalized earnings figure was |

| Peer comparisons | What a neighbor or fellow shop owner received | The exact earnings definition, add-back treatment, or WC peg in their deal |

| SourceCo buyer network data | What buyers in our automotive services network have paid for shops with comparable profiles | Covers adjacent automotive services; not a published dataset |The practical alternative to a benchmark: verify the inputs to your specific number rather than looking up a published output. Five comparability checks to run against any number you have heard:

A buyer who has looked at comparable shops can give you a range based on what they have actually paid for shops with your specific profile, not what a rule-of-thumb suggests.

A buyer building a model for a tire shop is running one calculation: does service labor revenue continue after the owner leaves, and what happens to tire margin if the supplier program does not transfer? Two shops at the same revenue with the same SDE can produce different offers because buyers answer that question differently for each shop.

"We run it at 60% GP, you know, 58 to 62%."

That is from an automotive services owner in the tire segment. Documented gross profit margins at that level, with records to support them, are exactly the asset quality signal buyers look for in a tire and mechanical shop.

[[definition-list: KPIs buyers track in a tire and mechanical shop]]

ARO (average repair order) | Average revenue per vehicle visit: total service sales divided by car count. In a tire-plus-service shop, ARO signals whether the shop captures full-car inspection revenue or primarily sells tires on price. A higher ARO with stable car count indicates pricing discipline and customer trust in the service lane.

Effective labor rate | Actual dollars billed per labor hour compared to the shop's posted rate. A persistent gap signals discounting or declined services. In tire shops where service margins carry the earnings profile, effective labor rate is a direct indicator of how much of the posted rate is captured as profit.

Bay utilization | The percentage of available bay-hours generating revenue. Low utilization at adequate car count typically signals a technician constraint, not a demand problem. Buyers model whether adding a technician would meaningfully increase earnings before the sale.

Technician depth and dependency | Whether production concentrates in one or two people. A shop where one technician drives 40% or more of service revenue carries key-person risk that buyers price through earnout conditions or transition requirements, based on SourceCo's analysis of buyer screens.

Inventory turns | The number of times per year total inventory is sold and replaced. Higher turns indicate that inventory is moving, aging risk is low, and the shop is not carrying dead product. Low turns signal aged inventory that will likely be subject to haircut at close.

Service and tire revenue mix | The ratio of service labor revenue to tire sales revenue. A shop generating 60% or more of gross profit from service labor is typically less dependent on tire margin and supplier program terms. Buyers will evaluate the service bay as the earnings engine and tire sales as the traffic driver.

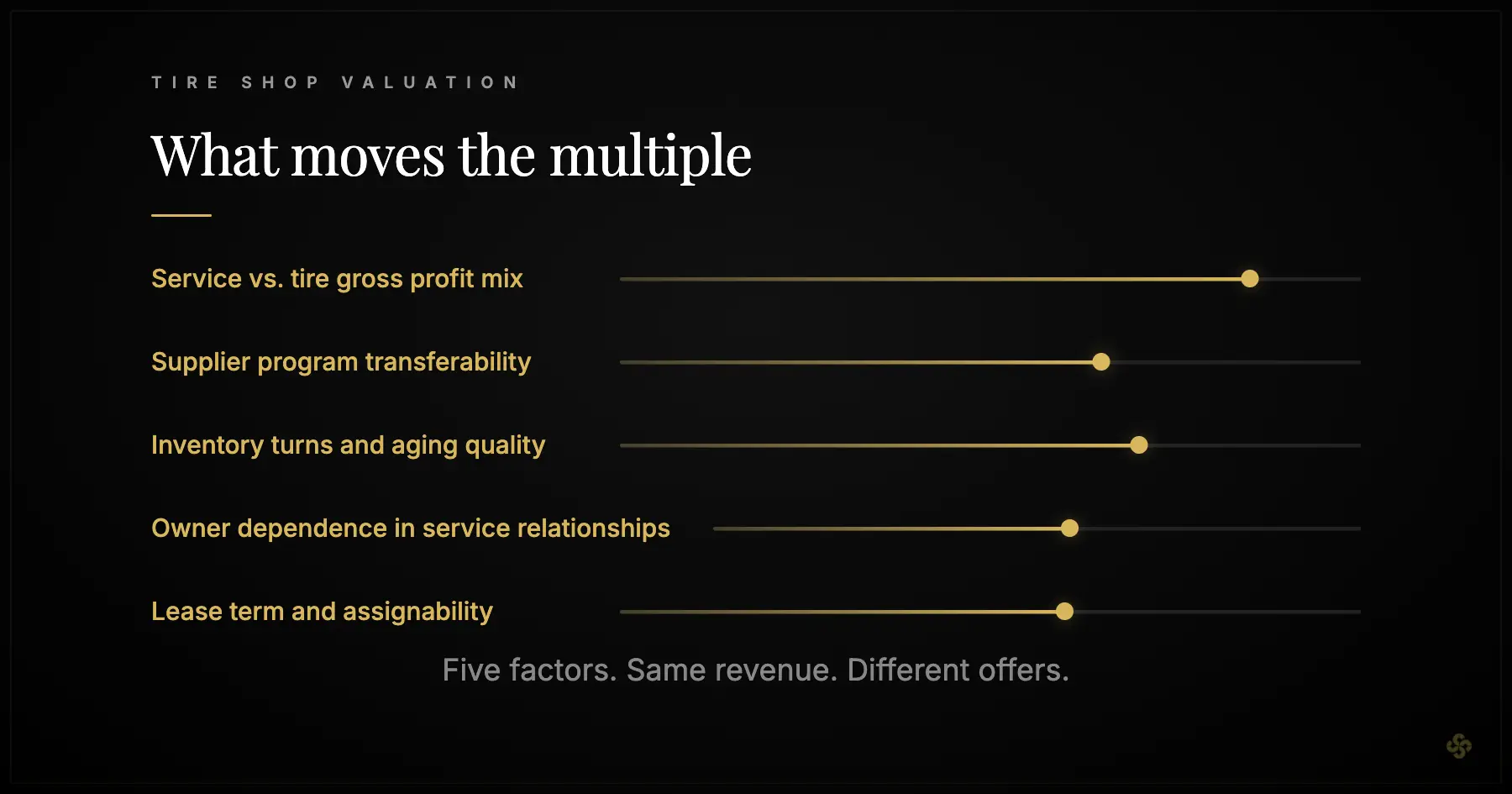

Fleet account concentration | The percentage of total revenue from commercial fleet customers. Fleet accounts signal recurring revenue but create single-account risk. A fleet account representing more than 20% of revenue typically results in tighter deal covenants or earnout conditions, based on SourceCo's analysis of buyer conversations in automotive services transactions.Based on SourceCo's analysis of buyer conversations in automotive services transactions, five factors consistently move the multiple within a size band for tire and mechanical shops:

Factor | What buyers read from it | Impact on valuation

Service/tire gross profit mix | Whether earnings come from high-margin service labor or thin-margin tire sales | Service-heavy mix supports the upper end; tire-margin-only depresses multiple

Supplier program transferability | Whether the incoming buyer can assume the current manufacturer agreements | Non-transferable programs are priced as revenue risk; may require earnout (proceeds contingent on post-close targets) conditions

Inventory turns and aging | Quality of physical inventory at close | Slow turns mean aged inventory and closing haircuts; affects actual proceeds, not headline

Owner dependence in service relationship | Whether key service and technician relationships are portable or owner-held | High owner dependence in service pricing or tech management triggers transition requirements

Lease term and assignability | Remaining term and landlord consent | Fewer than five years remaining with no options is a discount trigger; based on SourceCo's analysis of buyer screens

Different buyer types apply different weight to these factors. These frameworks reflect SourceCo's analysis of buyer conversations in automotive services transactions. Evidence for tire-specific buyer behavior is adjacent to mechanical and collision data.

Buyer type | Primary screen | What they underwrite | Post-close expectations

Operator buyer | Operational quality, technician and relationship stability | Current earnings without major restructuring required | 6 to 24 months; buyer takes over daily role

Multi-location platform | Management depth, inventory systems, supplier program quality | Scalable operations; documented processes; inventory controls | 3 to 12 months; integration into existing operations

Search fund or individual buyer | Clean SDE, defined transition, low owner-dependency in service | Earnings they can verify; documented supplier relationships | 12 to 24 months; buyer learns and takes over actively"I have two and three generations of families that come to me."

That is from an automotive services owner in the tire segment. Customer relationships that span generations are exactly what a buyer's model needs to trust that revenue is not owner-dependent: they are evidence that income continues not because the owner shows up, but because the shop is trusted.

[[cta-match]]

A retrade, a price reduction after the LOI citing issues found during diligence, in a tire shop transaction most commonly happens because of three things: inventory aging that was not disclosed, add-backs that cannot be supported, or a supplier program that cannot transfer to the new owner.

The quality of earnings review (an independent accounting examination of whether normalized earnings are accurate and repeatable) that institutional buyers commission after the LOI is signed will test every add-back and every normalization assumption. Commission your own earnings bridge before any buyer conversation begins. It is the same analysis, done earlier, when fixing problems costs nothing.

Financial records: Three to five years of federal tax returns; monthly P&Ls for at least 36 months; a one-page add-back schedule with documentation for each item.

Personnel: Technician and service staff roster with certifications, tenure, compensation, and owner-dependency assessment. Identify whether any single technician accounts for 40% or more of service revenue: buyers will ask, and the answer affects deal structure.

Inventory: A current, dated inventory list with units, cost, and age by SKU. Flag anything older than 12 months. Know your supplier's return policy for aged product before a buyer asks, and before the physical count.

Supplier programs: Copies of current manufacturer agreements with all terms. Confirm whether each agreement requires requalification by the incoming buyer. If the agreement is personal to you or your entity, the buyer will price that transfer risk.

Lease and facility: Current lease with all amendments and renewal options; confirmation that the lease can be assigned. Per SBA lender requirements and IBBA diligence norms, assignability must be confirmed before any LOI is signed, not during diligence.

Environmental: Phase I Environmental Site Assessment per EPA ASTM E1527-21 standards, required by virtually all institutional buyers and SBA lenders for facilities with used oil, refrigerant, waste tire handling, or underground storage. Commission your own Phase I before going to market so you control the findings and the timeline. A Phase I surfaced by the buyer's team during exclusivity gives the buyer a retrade opportunity you did not anticipate.

When buyers find problems in diligence, they do not always walk away. They restructure. An earnout (proceeds contingent on post-close targets) addresses supplier transfer risk. An escrow (proceeds withheld after close, typically 5 to 10%, released after 12 to 18 months) addresses undisclosed inventory issues.

A seller note (a loan from you to the buyer, repaid with interest) bridges a financing gap. Knowing these tools before diligence gives you options beyond accepting or rejecting a retrade. If you are at the point of thinking seriously about process, how to sell a mechanic shop covers the full sale sequence for mechanical shop owners.

[[cta-advisor]]

How do you value a tire business?

Tire business valuation starts with normalized cash flow: SDE for smaller owner-operated shops or EBITDA for larger managed ones, multiplied by a multiple that reflects shop size, risk, and buyer type. That produces enterprise value: the headline price before any deductions. Proceeds at close are reduced by outstanding debt, any working capital shortfall, transaction costs, and an inventory adjustment based on the physical count and aging at close. No publicly standardized tire-only EBITDA multiple exists; advisory sources publish directional ranges, but each shop is priced on its specific earnings profile.

How do you value a tire shop if inventory is a big part of the business?

Tire shop valuation starts with normalized cash flow (SDE or EBITDA) multiplied by a multiple. Inventory is then handled separately as a closing-day variable, not embedded in the multiple. At close, the buyer counts physical inventory and applies agreed adjustments for aging or slow-moving product. That count is compared against a target, and any shortfall reduces your proceeds directly. A shop with $180,000 in inventory at book but 40% aged over 12 months may receive significantly less than book value for that inventory at close.

What is a tire shop cash flow multiple and how is cash flow calculated?

The cash flow multiple is the number applied to normalized SDE or EBITDA to produce the headline enterprise value. Cash flow in this context is not net income from the tax return: it is normalized earnings after supported add-backs are applied. For a smaller owner-operated tire shop, SDE (which includes all owner compensation) is typically the starting metric. For a larger shop with a manager running day-to-day, EBITDA may apply. The multiple then reflects buyer type, shop risk profile, and earnings quality.

Do tire shops get valued on SDE or EBITDA, and when?

Smaller owner-operated tire shops, where the owner's compensation is the primary return, are typically valued on SDE. Larger shops with professional management and documented systems tend to see buyers use EBITDA. The threshold is not rigid: it depends on shop size, buyer type, and how central the owner is to daily operations. If the owner is also the service manager or parts manager, SDE is more likely the correct metric. If a hired general manager runs the shop without daily owner involvement, EBITDA applies.

How do working capital and inventory adjustments change what the owner takes home?

Both reduce proceeds below the headline enterprise value, and both are determined at or near close rather than at the time the LOI is signed. Working capital shortfall is the gap between the buyer's target and your actual working capital on closing day. Inventory adjustment comes from a physical count compared against an agreed aging schedule. Together, both adjustments reduced a $900,000 headline to $731,000 at close: from the same headline price, the same shop. Map both before evaluating any offer.

How do different buyer types value tire businesses differently?

Operator buyers focus on earnings quality and whether the shop runs without the seller's daily involvement. Multi-location platforms look for inventory systems, supplier program quality, and scalable operations they can integrate. Search fund buyers need clean SDE, a defined transition, and low owner dependency in key service relationships. Buyer type changes both the multiple discussion and the deal structure: earnouts and seller notes are more common with some buyer types. Based on SourceCo's analysis of buyer conversations in automotive services transactions, buyer fit matters as much as the headline offer.

What is the EBITDA multiple for a tire shop?

No named published dataset isolates tire-shop-specific EBITDA multiples as a distinct category with a stated sample size and date. Advisory firms publish directional ranges for automotive and tire businesses, but these should be treated as starting orientation rather than benchmarks. Actual multiples depend on shop size, earnings quality, inventory position, supplier program transferability, and buyer type. The inputs to your specific shop's number matter more than any published range.

Can I get an estimate of my tire shop's value before talking to buyers?

Yes. A private first-pass estimate requires two inputs: your normalized earnings and a brief description of the shop's profile. SourceCo can provide an earnings-based estimate in a single working session with no buyer outreach, no NDA required at that stage, and complete confidentiality. The estimate reflects what buyers in SourceCo's automotive services network have paid for shops with comparable profiles. It is the right first step before any external conversation begins.

What should I do if my inventory is aging before I go to market?

Work your supplier's return program first. Most major tire manufacturers have authorized return processes for current-account dealers. Returning aged inventory before a buyer's physical count reduces the adjustment that appears at close. If the product cannot be returned, price the haircut yourself before any LOI is signed: knowing the likely adjustment lets you negotiate the WC peg and inventory target from an informed position rather than discovering it at the closing statement.

A broker estimate, a peer's figure, or a benchmark range becomes a real number only when the earnings metric is confirmed, the add-backs are documented, the inventory position is understood, and the working capital target is mapped against your actual balance.

Most of that work can be done privately before any buyer conversation begins. Doing it first is the difference between a number that holds at closing and one that changes at the closing statement.

[[cta]]

Free Valuation Tool

.svg)

Before you contact a single buyer, get a first-pass estimate of what your shop could be worth. It takes two minutes and requires no outreach, no disclosure, and no commitment to a process.

Get Your Free Valuation

.svg)

Confidential & Free

.svg)

Before you contact a single buyer, get a first-pass estimate of what your shop could be worth. It takes two minutes and requires no outreach, no disclosure, and no commitment to a process.

Talk to an Owner Advisor

Active Buyers

.svg)

Match with pre-screened buyers from our network of 4,000+ active acquirers - see who is looking for a business like yours instantly.

See Who is Buying

.svg)